In the decade since the Paris Agreement was signed, the pipeline of planned coal capacity has collapsed worldwide. No New Coal has become the norm across the world: 164 countries have no prospective coal capacity, and stalled and cancelled coal proposals have led to a record low in the number of countries proposing or building new coal plants. However, a small group of countries continue to keep new coal on the table and threaten progress.

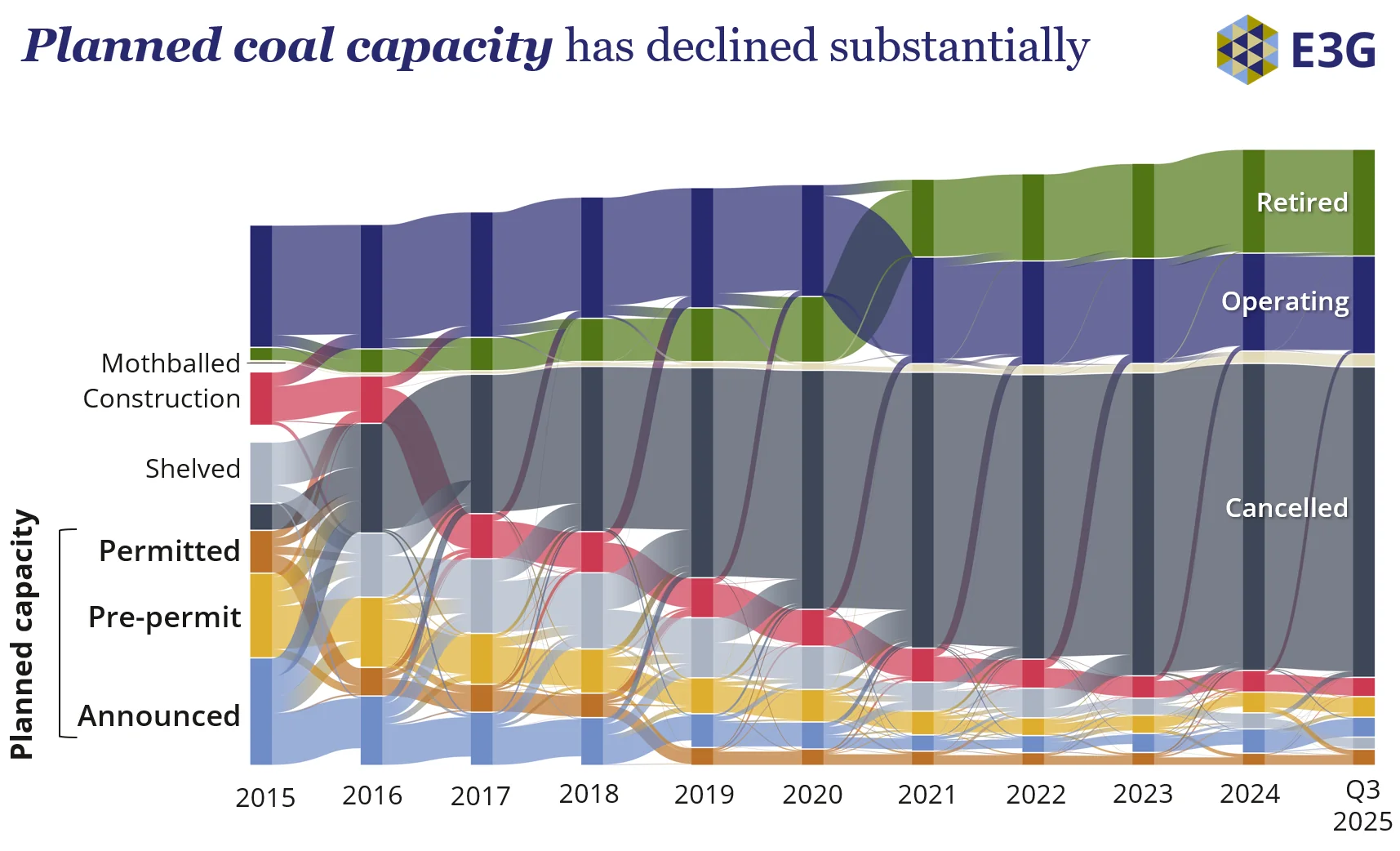

While planned coal power has fallen by 65% since 2015, prospective capacity is still over 400 GW. China in particular remains a global outlier, accounting for over 60% of planned capacity, despite its unparalleled rollout of clean energy making new coal power unnecessary. As countries look to COP30 and to addressing the expected emissions gap, the final push towards No New Coal remains key.

In our briefing, we set out progress on achieving No New Coal and highlight the challenges that still must be addressed to ensure a just, effective transition away from coal and, ultimately, all fossil fuels. [1]

No New Coal is now a global norm for the vast majority of countries

- 164 countries – covering more than two-thirds of the global economy – either have no planned coal in their project pipeline and/or have made a No New Coal commitment.

- The global pipeline of planned coal-fired power plant projects has collapsed by 65%, and 74% when excluding China, in the decade following the ratification of the Paris agreement. The shift is made possible by the growth of renewables. Solar and wind accounted for 87% of new capacity additions in 2024, while coal made up just 3%.

- Just 11 countries now account for 96% of new planned coal power. The remaining 4% is spread across 18 countries. This total of 29 countries still planning new coal is down from 65 a decade ago. In almost all of the countries still planning coal power, solar and wind capacity additions are exceeding coal and gas.

- Momentum on No New Coal continued in 2025 NDCs: Australia, Cambodia, Canada, Mauritius, Morocco, Singapore and the UK reiterated or made commitments to no new coal (see our NDC energy commitments tracker); Thailand cancelled its last planned coal plant; and Honduras committed to stop permitting new coal plants through new membership of the Powering Past Coal Alliance (PPCA).

- Approximately 4 billion tonnes of CO2 emissions have been avoided every year of the last decade thanks to the collapse of planned coal capacity – equivalent to nearly one-third of China’s annual CO2 emissions.

OECD and Latin America pushing ahead

- There is now no actively planned coal on the entire continent of Latin America. As COP30 President, Brazil has the opportunity to reaffirm this milestone. Faced with the urgent task of addressing the NDC emissions gap, formally committing to No New Coal would reflect the reality of Brazil’s energy plans and send a clear signal that moving beyond coal is a key action to implementing and exceeding NDCs.

- Proposals for new coal power capacity among countries in the OECD and EU have collapsed by 97% since the adoption of the Paris Agreement. No new coal projects have entered construction anywhere in the OECD since the end of 2019. The world’s wealthiest countries are now looking to phase out coal entirely.

- There is a major opportunity for Türkiye to formalise its de facto halt on new coal projects to build credibility in its COP31 Presidency bid and channel investment for clean energy. A formal commitment to No New Coal from Australia can also pave the way for bigger coal-to-clean ambition ahead of a potential joint COP31 Presidency with Pacific Island States. In Japan, the newly elected government must either decline the permit of its last proposed coal-fired power station, or ensure the project developers plan for full abatement in line with the IPCC standard of at least a 90% CO2 capture rate.

Planned coal levelling off outside the OECD; China remains an outlier

- Outside the OECD (excluding China), the number of planned coal projects has largely levelled off, with many shifting investments towards renewables. A few countries, such as India, Indonesia, and Zimbabwe, continue to expand their coal pipelines.

- Realising President Prabowo’s clean energy vision for Indonesia – based on announcements to close Indonesia’s coal fleet within 15 years, achieve 100% renewable energy by 2035, and install 100 GW of solar power – requires a clear signal that only new renewables capacity is going to be prioritised going forward. Committing to No New Coal provides such a signal. Pakistan’s solar boom presents a clear opportunity to end the country’s reliance on new coal power and fulfil the former Prime Minister’s 2020 announcement that Pakistan would “not have any more power based on coal”. As the incoming ASEAN chair, the Philippines can also use a firmer No New Coal commitment to enable regional planning on coal-to-clean transitions.

- African leaders’ call for a rise in the continent’s share of global renewable energy investments from just 2% today to at least 20% by 2030, must be met to ensure there is no pursuit of coal in Africa.

- China remains a global outlier: responsible for 62% of the world’s planned coal capacity. However, the country is also the world leader in the rollout of both wind and solar, with 1,215 GW of prospective capacity and a commitment to increase this pipeline to over 3,600 GW by 2035. There is no need for new coal: in the first half of 2025, generation from clean energy exceeded domestic demand growth. Going beyond its insufficient NDC, China now has a clear opportunity to implement plans to end new coal construction in its next Five Year Plan in 2026.

[1] All data in the briefing, unless otherwise referenced, is from GEM (2025), Global Coal Plant Tracker – July 2025 release. When analysing changes in prospective capacity since the Paris Agreement was signed, data from January 2016 is used as the starting point. This is referred to as “since 2015” or “in the last decade”.