The sharp decline in European oil and gas demand over the next 25 years will deprive many of the EU’s key fossil fuel suppliers of significant income and foreign currency flow. Without sufficient support for an equitable transition, countries heavily reliant on oil and gas revenues will face economic and political turmoil, creating new security risks for the EU. The EU needs to redefine its relationships with its vulnerable suppliers to mitigate these risks in this crucial decade.

At COP28 in Dubai last year, nearly 200 countries committed to transitioning away from fossil fuels. The “UAE consensus” provided a political framing to the real economy trend: renewable energy is growing at unprecedent rates, and fossil fuel use is set to peak by 2030, according to the International Energy Agency. This peak may even occur within the next couple of years if the world’s largest economies meet their existing climate and energy targets.

Oil and gas demand in the EU is already in structural decline, according to the bloc’s own projections. By 2030, demand will fall by a quarter and half, respectively, compared to 2019 levels. By 2050, demand for both fuels will reduce by at least 80%. EU’s oil and gas suppliers stand to lose their most crucial export market and revenue as the transition progresses, and few will be able to find alternative buyers in the medium term. If they don’t succeed in diversifying their economy, falling oil and gas revenues will compromise economic, social and political stability.

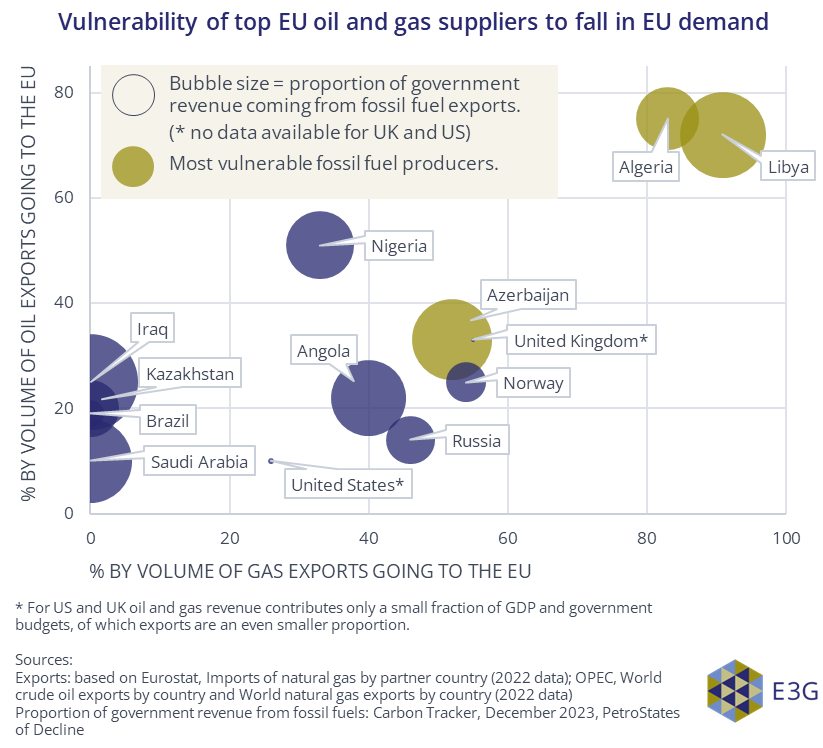

In this briefing, E3G identifies Libya, Algeria and Azerbaijan as particularly vulnerable due to their reliance on the EU for export revenues (“exposure”) and their lack of ability to diversify their economies (“resilience”), as well as underlying political, social, and demographic tensions.

Figure 4: Of the top oil and gas suppliers to the EU, Libya, Algeria and Azerbaijan are most vulnerable to a fall in demand from the EU. While Nigeria is also a vulnerable supplier it is not connected to the EU by pipeline or as geographically close – and so it is better placed to find alternative markets.

The EU and member states must support these countries transition away from fossil fuels, or risk destabilising its neighbourhood, with consequences extending beyond energy policy. Disruptions could affect migration flows, trade, and geopolitical stability in regions that have long supplied Europe with energy.

Key recommendations to the EU and member states:

- Transparent communication: The EU must clearly communicate its oil and gas demand reduction trajectories to key suppliers, helping them avoid stranded assets and direct investments toward more sustainable sectors.

- Energy resilience over diversification: Rather than simply diversifying its fossil fuel suppliers, the EU should focus on reducing overall demand, building out renewables and bolstering its resilience to market volatility.

- Support for economic diversification: The EU should initiate transition dialogues with Algeria, Libya, and Azerbaijan to co-develop strategies that reduce their dependence on oil and gas revenues and foster new trade and energy relationships.

- Alignment with regulatory mechanisms: Partnerships with key suppliers should be rethought in light of the EU’s climate regulations, such as the Carbon Border Adjustment Mechanism and the EU Methane Strategy.

- International support for transition: The EU should back initiatives like the Beyond Oil and Gas Alliance to foster successful transitions and inspire confidence in other suppliers.

- Unlock clean growth: The EU should use its dialogues with China, the Gulf Cooperation Council and other partners to leverage wider investment and technical support needed to create clean growth opportunities in supplier regions.