The following report, written in partnership with Sandbag, assesses the impacts and risks of the EU’s proposed carbon border adjustment mechanism (CBAM). The impact of the likely CBAM will be minor: the CBAM only covers 3.2 percent of goods imported into Europe, but 47 percent of the free emission allowances currently given to industry.

On 14 July 2021, the European Commission put forward its proposal for a carbon border adjustment mechanism (CBAM), a mechanism that would put a carbon levy on imports of certain emission-intensive products from third countries into the EU. This is part of the ‘Fit for 55’ package, a group of 12 directives and regulations aiming to achieve 55% emissions reductions compared to 1990 levels.

The introduction of a CBAM was first presented by the European Commission as “an alternative to the measures that address the risk of carbon leakage in the EU’s Emissions Trading System”.

Different stakeholders, including policymakers in the European Commission and EU Member States, the European Parliament, industries, and EU’s trade partners, hold different positions on what the CBAM should try to achieve. These competing views will be brought to bear in the legislative process to come and will impact the final design of the CBAM, which is due to be fully implemented by 2026 following a three-year transition phase beginning in 2023.

The CBAM, if implemented in its current proposed form, will raise the cost for EU importers of some Chinese goods to access the European market. But the overall impact is likely to be small as the current proposal only covers a small share of Chinese exports to the EU, and importers will recover most of the additional costs through higher prices in EU markets.

Key findings

- The EU’s CBAM proposal comes at a time of increased international trade tensions, which the EU aims to tackle through a variety of trade policy instruments. Against the background of tightened EU scrutiny on foreign investment and trade, CBAM has been interpreted by some of the EU’s trading partners as a tool to protect the single market disguised as climate policy. However, the motivations of the EU’s CBAM are multi-faceted.

- Different EU actors associate a range of different objectives with the CBAM. Some European stakeholders see the CBAM as a way to prevent ‘carbon leakage’; others see it as a way to drive climate ambition globally; a means to raise new revenues, by replacing the handing out of free allowances to EU industries under its emissions trading scheme (ETS); a way to raise the price of polluting products in the internal EU market to make less polluting products more competitive; others, especially some industry stakeholders, view the measure as a solution to address their competitiveness concerns linked to rising climate ambition in the EU.

- There are different design options for the CBAM. Choices include: the sectoral and emissions scope, compliance instruments, carbon content assessment, possible exemptions, the use of revenue and the treatment of the EU’s exports regarding possible discounts on their carbon costs. However, no matter which design will be chosen for the final CBAM, the EU institutions have stressed the importance of compliance with WTO rules.

- The current proposal envisions a narrow sectoral scope, covering direct emissions only (“scope 1” emissions), with the possibility to submit verified calculations or use default values and with revenues envisioned for EU own resources without earmarking. A three-year trial period will exempt importers of any charge.

- The legislative timeline suggests that the CBAM will come into force earliest in the beginning of 2023, following scrutiny and political discussions by the European Parliament and the Council, with consultations by the European Commission with trade partners. The trial period will run between 2023-2025 during which importers would not face extra cost from the CBAM. The full price signal of the CBAM will not be applied to importers of goods from the EU’s trading partners until 2035 when free allocation is proposed to be fully phased out.

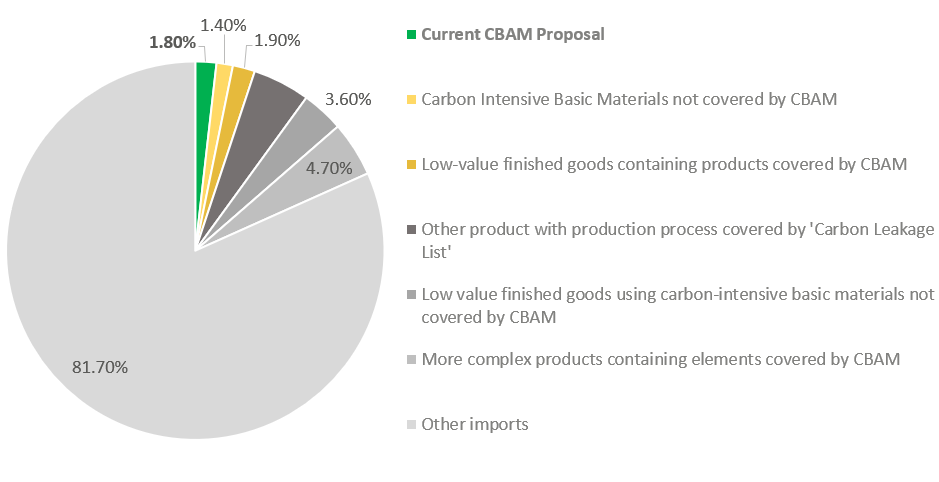

- The impact of the likely CBAM scenario on Chinese exports to the EU is minimal. The sectors covered by the current CBAM proposal represented 1.8% of Chinese exports to Europe in 2019, in value. Potential extensions could increase that share to 5% in an extreme scenario.

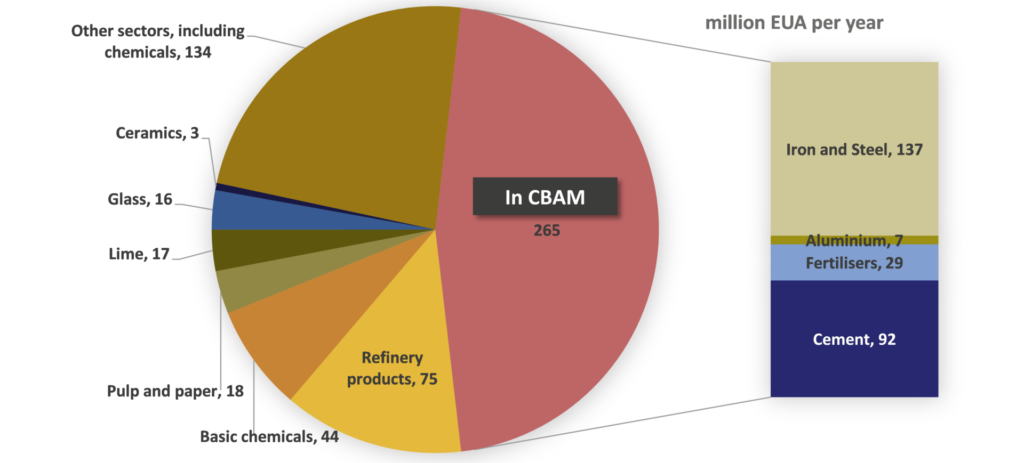

- Despite its narrow coverage, introducing the CBAM could allow the EU to phase out the free allocation of 265m emission permits under its carbon market, worth €15.9bn, every year.

- The EU’s top trading partners have been paying close attention to the CBAM conversation in Europe. Some partners are interested in exploring the feasibility of CBAMs, including the US and Canada, while other countries in the EU’s neighbourhood and OECD countries are aiming to comply with a CBAM through exploring the development of domestic carbon pricing schemes. But many, particularly those in the developing world, are raising concerns on its design, fairness, and feasibility.

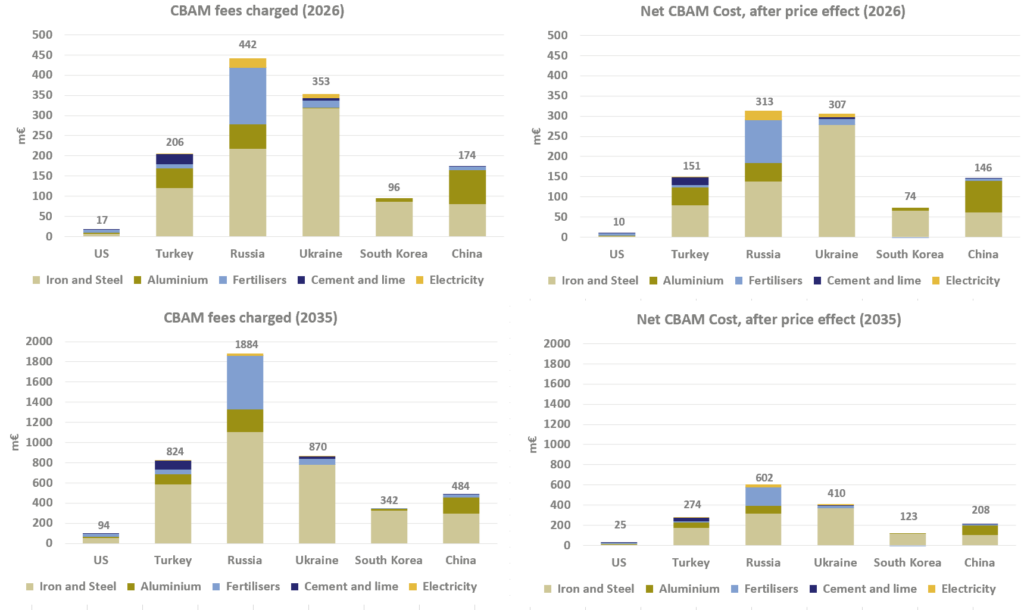

- The new cost to EU and foreign industries will likely be passed on to the direct consumers of the products covered in the CBAM, so that part of the cost will be recovered by importers in the form of higher selling prices for their products. The overall net effect on importers is likely to be very small. The net CBAM cost for importers, which factors in the recovery through higher market prices is significantly lower than the CBAM fees. Overall, the total net CBAM cost should barely reach €1.0bn in 2026 and €1.6bn in 2035 across imports from six major trading partners.

- The CBAM mainly raises redistribution issues within the EU itself, as its introduction will raise revenues but its costs will largely be borne by consumers. It is also likely to raise opposition from the EU industries using the goods covered by the measure, which will likely become more expensive, although only marginally.

- Phasing out the free allocation of emission permits to industry is inevitable in the long run, as the EU reduces its cap on emissions. If the CBAM was not introduced, alternatives could include a combination of heavily subsidised decarbonisation efforts within the EU and the subsequent application of product requirements which would apply to imports as well as domestic production.

- To accelerate the uptake of low-carbon technologies to address the climate crisis amid geopolitical and trade tensions, countries would need to introduce a suite of measures beyond the CBAM, such as product requirements, environmental standards in government procurement schemes and regional trade agreements, to facilitate the trade of low-carbon technologies in order to meet climate goals while safeguarding national interests.