The USA has the largest coal phase out challenge of all the G7 countries given the scale of its existing coal use but it is making the most positive progress so far. New policies have been introduced to capitalise on shifting market dynamics. The USA has also led international efforts to restrict financing for unabated coal plants.

The USA is ranked #1 in the E3G G7 coal phase out scorecard.

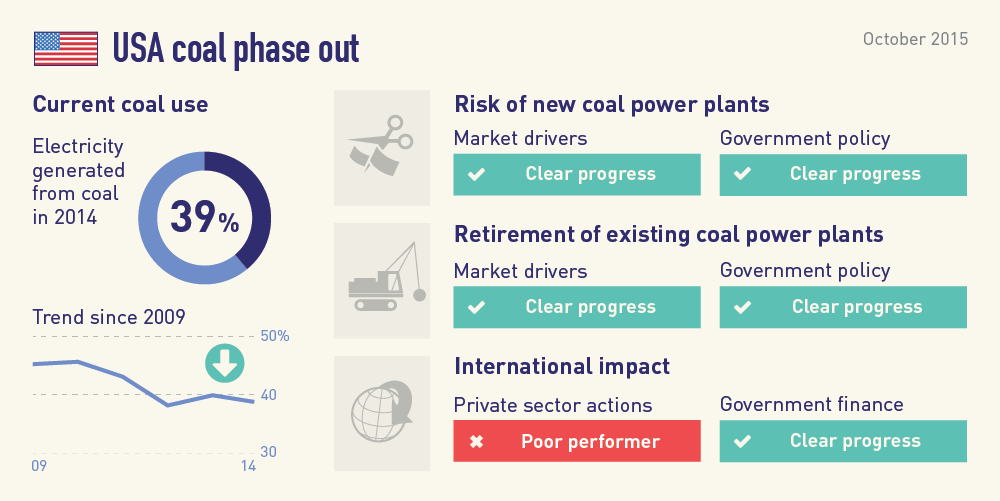

The United States has 288GW of coal power generation capacity, more than double the total capacity of the other six countries combined. However, coal use is on a clear downward trend, with less than 40% of US electricity generation coming from coal.

Risk of new coal power plants

Since 2005, 184 proposed new coal plants, valued at $273bn, have been cancelled at various stages of development. With the exception of a demonstration coal gasification plus CCS project, no new coal plants have broken ground since November 2008. There is now less than 5 GW of new coal plants in the development pipeline, with 4 of these 7 projects seeking to develop CCS with Federal support. The market for new unabated coal plants has ended, while the EPA’s new source standards will require any new coal plants to operate with CCS technology or natural gas co-firing, bringing an end to new unabated coal.

Retirement of existing coal power plants

Since the start of the Obama Administration, new federal and state level regulations have been introduced to mitigate the significant health and climate costs associated with coal combustion. In addition to existing Mercury Air Toxics Standards (MATS) and state-level Renewable Portfolio Standards, the EPA’s proposed emission standards for existing power plants under its Clean Power Plan will enter into force in 2022.

Reduced costs of renewable technologies and natural gas have combined to make ageing coal plants uneconomic. Retirements of existing coal plants are subsequently gathering pace, with 84GW already confirmed for retirement and 100GW of closures anticipated before the end of the decade.

International impact

With respect to international impact, the USA is again the most positive performer, thanks to its leadership of efforts to restrict finance for unabated coal plants. This includes its positions on bilateral development assistance, multilateral development banks and OECD export credit policies. Notably, in September 2015, the USA and China announced a set of actions on climate change, including that China would ‘strictly control’ domestic and international financing of high-carbon projects.

The performance of the USA is, however, more negative in respect to its position as the world’s fourth largest coal exporter and the continued support of US banks for coal projects internationally. During 2015, both Citigroup and Bank of America have taken steps to reduce financial support for coal mining but the banking sector is yet to sufficiently address financial support for coal power generation projects.

Actions required

When considering immediate actions for the G7 to take before the close of 2015, the USA is in a privileged position having implemented a wide-ranging set of policies during the year to date. While these are a positive foundation, the USA still has a long way to go to complete its coal phase out.

Policies will need to be further strengthened in the years ahead. The USA should therefore take the opportunity now to find transition pathways for coal-producing regions. This should include addressing the risk of increased coal exports and the impact of coal production from Federal lands.