European energy-intensive industries are going through their most uncertain time since the 2008 financial crisis. Despite a growing consensus that their future hinges on decarbonisation, a stalling project pipeline is undermining delivery. A series of legislative proposals under the Clean Industrial Deal (CID) coming over the next year can deliver the concrete changes that European industry desperately needs.

Europe’s future industrial competitiveness hinges on decarbonisation

The EU’s industrial base drives prosperity by fostering innovation, creating quality jobs, and supplying key inputs for other sectors, but it now faces rising costs, global competition, and looming reinvestment deadlines. As a result, competitiveness has moved to the core of Europe’s political agenda, with climate action increasingly reframed as a foundation for long-term prosperity rather than a constraint.

Many companies have already planned low-carbon investments, showcasing Europe’s leadership in clean technologies. Yet weak demand, high energy costs, and insufficient financial support are hindering final investment decisions. With projects outside the EU advancing faster, Europe risks losing its first-mover advantage.

Making industrial decarbonisation bankable through electrification, demand-creation and funding

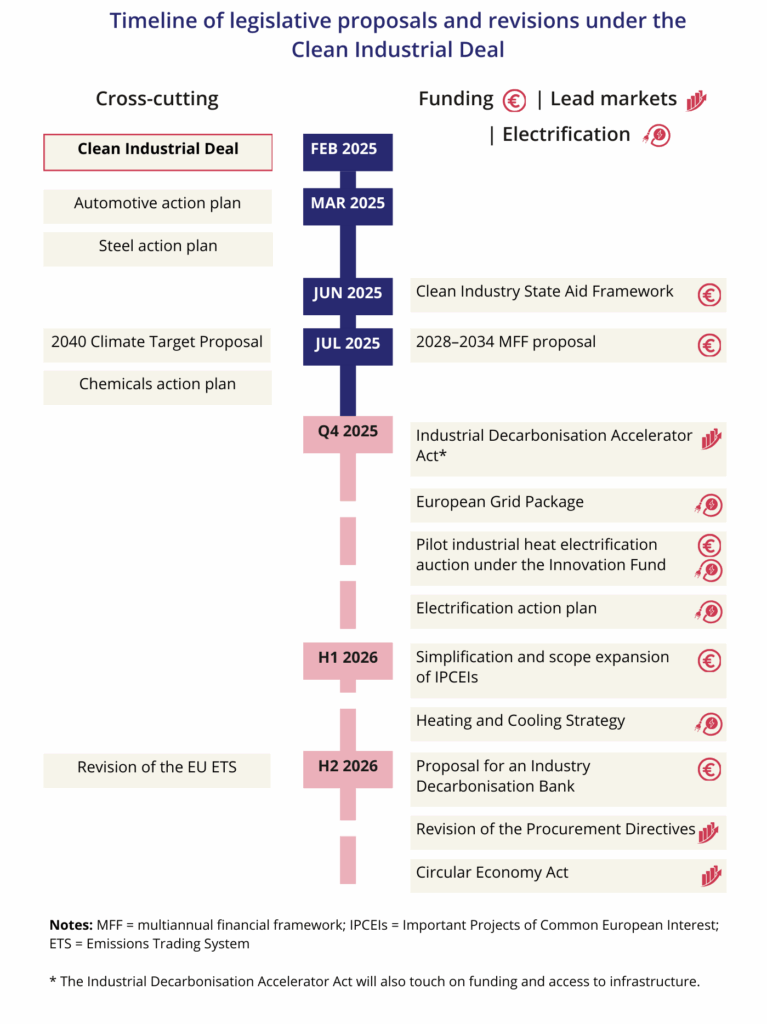

The coming year will see a series of major proposals and legislative revisions as part of the Clean Industrial Deal. They must deliver a compelling business case that unlocks investment, drives industrial renewal and positions Europe at the forefront of future-proof technologies.

Informed by E3G’s in-depth knowledge of the production and demand landscape for the steel, cement and chemical sectors, this briefing focuses on the decisions most critical to making industrial decarbonisation investable.

We offer recommendations for European legislators on three priority areas:

- Unlocking direct electrification. Supercharge industrial electrification by upgrading grid governance, cutting electricity costs through fairer taxation and charges, and hard-wiring electrification into EU strategic priorities and funding to fast-track high-impact projects.

- Creating lead markets. Kick-start demand through a comprehensive lead markets strategy under the upcoming Industrial Decarbonisation Accelerator Act (IDAA). This strategy should combine product standards, demand-side obligations and smart incentives to grow both public and private markets for clean and circular products.

- Aligning and scaling funding for deployment. Focus scarce EU funds to de-risk first movers, finance enabling infrastructure and build early markets. Use the Competitiveness Coordination Tool, announced under the Competitiveness Compass, to unite EU and national resources behind strategic, including cross-border industrial projects.

Together, these levers can make industrial decarbonisation a bankable proposition in Europe – but only if anchored in regulatory stability. Europe’s predictable climate and policy framework is one of its strongest competitive advantages. Dismantling it now would punish early movers, reward inaction and inject damaging uncertainty just as companies are deciding whether to reinvest in Europe.

Figure: The legislative timetable for the remainder of 2025 and into 2026 offers significant scope to build in targeted actions to unlock direct electrification, build lead markets, and align and scale funding for deployment.

Data used in this briefing are sourced from the Global Project Tracker by our partner, the Mission Possible Partnership. You can access the tracker directly at the Mission Possible Partnership’s website here: https://tracker.missionpossiblepartnership.org/mpp-global-projects-map/pipeline