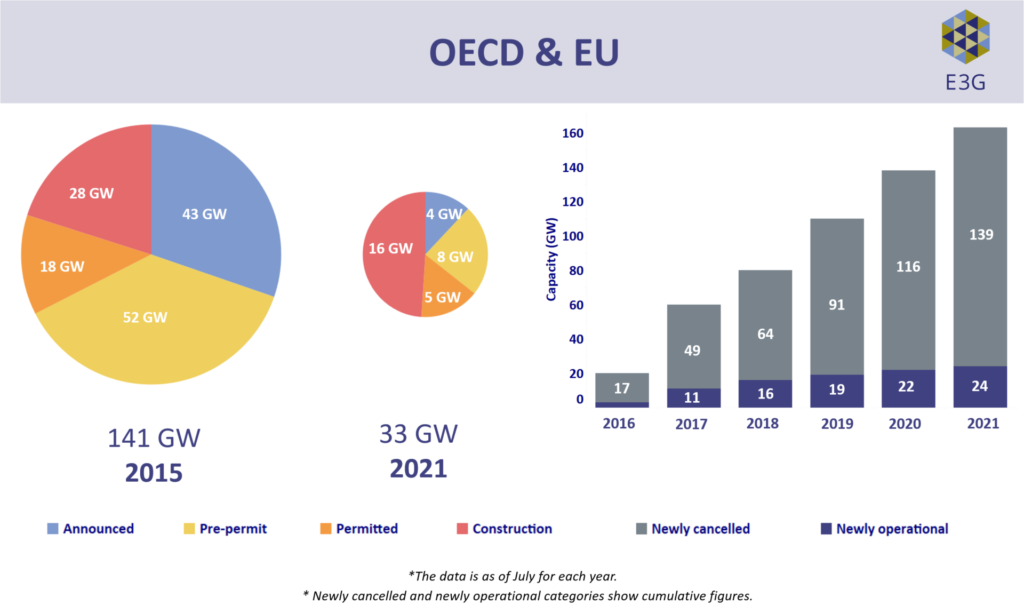

- The new coal pipeline in OECD & EU has collapsed by 85% since 2015, with 139GW of projects cancelled.

- Cancellations outnumber new plants entering into operation by 6:1.

- The OECD & EU is now home to just 6% of the remaining global pipeline.

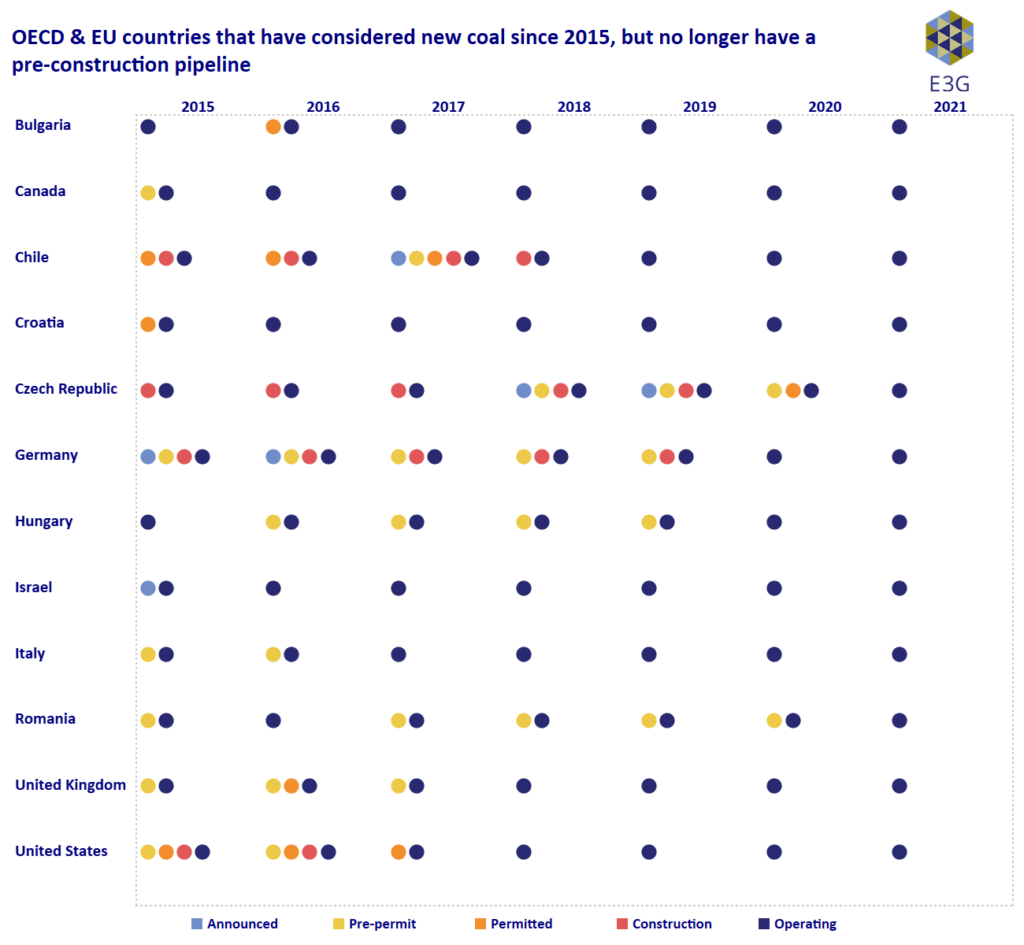

- 12 OECD & EU countries have considered new coal projects since 2015 but no longer have projects under development.

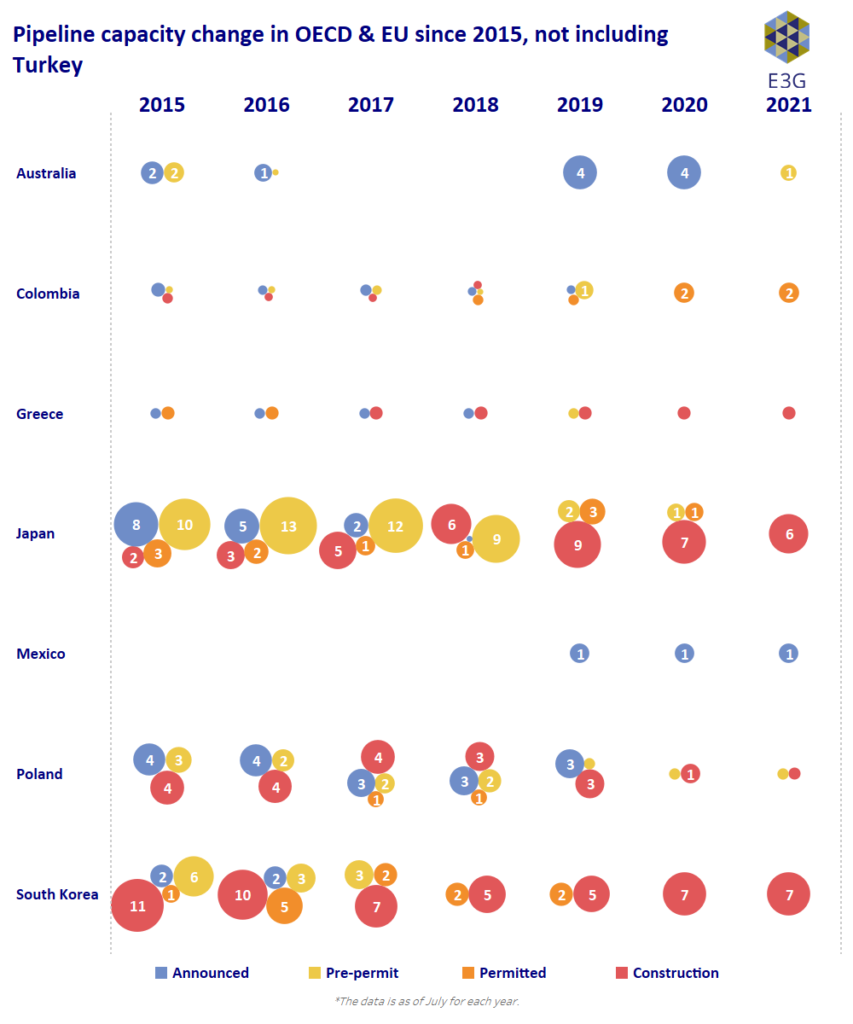

- Five OECD & EU countries have coal projects in the pre-construction pipeline; all are unlikely to proceed.

Figure 1: Reduction in size of the OECD & EU coal project pipeline (left) and year-on-year tracking of projects that were cancelled or newly operational (right). Click to expand.

The primary coal transition dynamic underway across the OECD & EU is the accelerating retirement of existing coal power generation, with 56% of capacity either closed already since 2010 or scheduled to close by 2030.

This dynamic is also reflected in respect to the collapse of the new coal pipeline. Almost four-fifths of OECD & EU countries have either formally committed to no new coal (64%) or have no projects under development (14%). This includes 12 countries that have considered new coal power generation since 2015, but which no longer have projects under development, as shown by Figure 2 below.

Figure 2: OECD & EU countries that have considered new coal since 2015, but no longer have a pre-construction pipeline, as of July 2021. Click to expand.

Since 2015, just 24GW of new projects entered operation across the OECD & EU, compared to139GW that were cancelled, giving a ratio of nearly 6:1. Only a handful of projects remain that have been proposed but have not yet entered construction, in Australia, Colombia, Mexico, Poland and Turkey. (Figure 3).

Figure 3: Pipeline capacity change in OECD & EU since 2015, not including Turkey. Click to expand.