The global pipeline of proposed coal power plants has collapsed by 76% since the Paris Agreement in 2015, bringing the end of new coal power construction into sight.

Figure 1: Sankey diagram showing global changes in capacity status, 2015-2021. Note that graphic does not include projects that did not change status over this period.

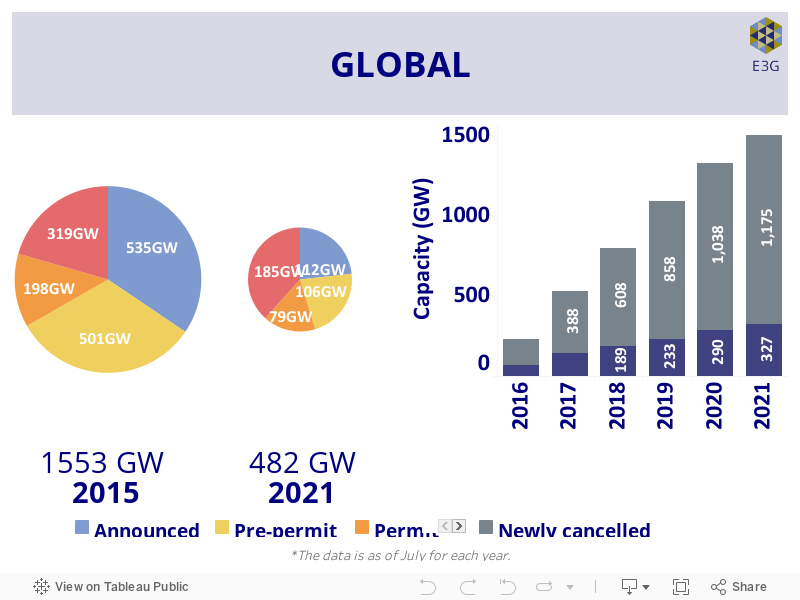

Figure 2: Reduction in size of the global coal project pipeline (left) and year-on-year tracking of projects that were cancelled or newly operational (right). * The data is as of July for each year. * Newly cancelled and newly operational categories show cumulative figures.

United Nations Secretary General Guterres has called for ‘no new coal by 2021’, while COP President Designate Alok Sharma has called for COP26 in November 2021 to ‘consign coal to history’. COP26 provides the ideal moment for governments to turn off the tap of new coal construction.

Since 2015, 44 governments (27 in the OECD & EU, 17 elsewhere) have already committed to no new coal, opening a pathway for remaining countries that are yet to act. We find that a further 40 countries (eight in the OECD & EU, 32 elsewhere) are without any projects in the pre-construction pipeline and are in a position where they could readily commit to ‘no new coal’.

Globally, 1,175GW of planned coal-fired power projects have been cancelled since 2015. Accelerating market trends have combined with new government policies and sustained civil society opposition to coal. The world has avoided a 56% expansion of the total global coal fleet (as of June 2021), which would have been equivalent to adding a second China (1,047GW) to global coal capacity.

As of July 2021, China and the countries with the next five biggest pre-construction pipelines (India, Viet Nam, Indonesia, Turkey, and Bangladesh) account for over four-fifths of the world’s remaining pipeline. Action by these six countries could remove 82% of the pre-construction pipeline. The remaining pre-construction pipeline is spread across a further 31 countries, 16 of which have just one project. These countries could follow global momentum and many of their regional peers in ending their pursuit of new coal-fired power generation.

The dynamic within the OECD & EU has already moved on to accelerating the retirement of existing coal power generation, with 56% of operating capacity either closed already since 2010 or scheduled to close by 2030. The pipeline of proposed coal power plants in OECD & EU countries has collapsed by 85% since 2015. The remaining proposed projects in OECD & EU countries make up just 6% of the global pre-construction pipeline. Australia, Colombia, Mexico, Poland, and Turkey are under pressure to follow their OECD & EU peers.

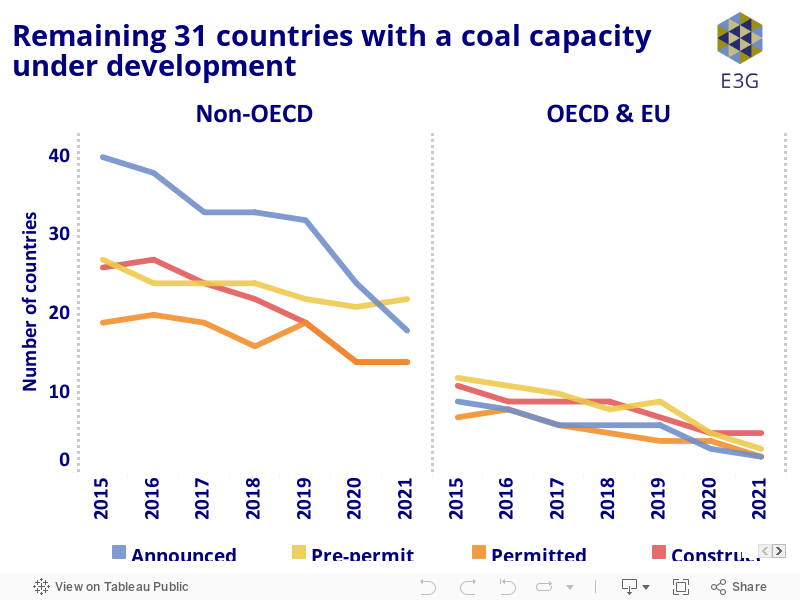

Figure 3: Declining numbers of countries with a coal pipeline within and outside the OECD & EU since 2015, by pipeline status.

Among non-OECD countries (excluding China), the pre-construction pipeline has collapsed by 77% since 2015, with a cancellation ratio of over 5:1. 27 countries have ended the development of new coal power generation through project cancellations and / or policy commitments since 2015. This shift away from coal is being reflected in governments’ political commitments, policy frameworks, and NDC submissions, for example in Pakistan, Malaysia, and Sri Lanka. They are serving as regional pathfinders that other countries can follow.

The group of non-OECD countries is home to 39% of the remaining global pre-construction pipeline, 80% of which is located in just nine countries. Four of these governments (Bangladesh, Pakistan, Indonesia and Viet Nam) have already indicated some form of restriction on new coal construction, which can be further clarified and tightened ahead of COP26. The remaining 20% of the non-OECD pipeline is spread across small projects in 22 countries, many of which could readily commit to no new coal and pursue clean alternatives instead.

The international community can further support these countries in moving away from coal through provision of public and private clean energy finance; support to develop flexible grid infrastructure; and technical and capacity assistance to bolster regulatory and policy frameworks that accelerate the transition from coal-to-clean. COP26 will be a key moment for OECD & EU members and China to demonstrate that such support is available now for all countries that are willing to shift from dirty coal to clean energy.

China alone is home to almost 53% of the capacity under construction and 55% of the pre-construction pipeline. China has, however, seen a 74% reduction in the scale of its project pipeline, with 484GW of cancellations since Paris. President Xi has announced an intention that China will ‘strictly control’ new coal growth, but this has yet to be reflected in sectoral Five-Year Plan (FYP) policies. China is also isolated as the last remaining major provider of public finance for overseas coal projects, following Japan and South Korea’s recent commitments to end coal finance. An end to Chinese finance would facilitate the cancellation of over 40GW of pipeline projects in 20 countries.

The collapse of the global coal pipeline and the rise of commitments to ‘no new coal’ are progressing hand in hand. Ahead of COP26, governments can collectively respond to UN Secretary General Guterres’ call for ‘no new coal by 2021’. Global trends are positive: governments can seize this moment to confirm their commitment to move from coal to clean energy.

You can also explore the report’s findings through the following geographical breakdowns:

- The new coal pipeline in OECD & EU has collapsed by 85% since 2015, with 139GW of projects cancelled.

- Cancellations outnumber new plants entering into operation by 6:1.

- The OECD & EU is now home to just 6% of the remaining global pipeline.

- 12 OECD & EU countries have considered new coal projects since 2015 but no longer have projects under development.

- Five OECD & EU countries have coal projects in the pre-construction pipeline; all are unlikely to proceed.

- The pipeline of proposed coal power plants in non-OECD countries (excluding China) has contracted by 77% since 2015.

- 552GW of coal power projects were cancelled over this period, compared to 105GW which went into operation; a ratio of 5.3:1.

- 27 non-OECD countries that had previously considered new coal power generation no longer have any projects in the pipeline.

- The 189GW of projects remaining as of July 2021 is heavily concentrated, with 80% locatedin just nine countries.

- South-East Asia (42%), South Asia (32%) and Sub-Saharan Africa (13%) collectively account for 87% of the non-OECD pipeline.

- China accounts for 55% of the world’s pre-construction pipeline (163GW), in addition to hosting over half of the world’s operating coal fleet.

- China has, however, seen a 74% reduction in the scale of its project pipeline, with 484GW of cancellations since Paris.

- Project cancellations outnumber newly operational capacity by 2.4:1, a much lower figure than in the rest of the world.

- Coal industry groups have proposed expanding coal capacity by a further 350GW, but recent analysis showsthat China can meet its energy security goals with no net new coal, keeping its emissions goals on track.

- China is isolated as the last major provider of public finance for overseas coal plants, with over 40GW of coal in 20 countries in the pre-construction pipeline.

- South Asia has a pre-construction pipeline of 37.4GW, with India’s 21GW pipeline accounting for 56% of this.

- The pipeline has contracted by 87% since 2015, with cancelled capacity outnumbering capacity going into operation by a ratio of 6.6:1.

- Three out of four countries in South Asia (Sri Lanka, Bangladesh and Pakistan) are showing leadership in cancelling projects and making political statements that they will no longer pursue new coal power.

- Significant socio-economic headwinds to new coal in India have led to State-level commitments to no new coal, opening a pathway for national progress.

- South-East Asia has seen a 63% decrease in the scale of the pipeline of proposed coal power plants since 2015.

- This represents a ratio of 3.1:1 between projects cancelled (102GW) and those that went into operation (33GW).

- The remaining 49GW of pre-construction pipeline is spread across seven countries. This is 42% of the non-OECD and 16% of the global pipelines.

- Regional leaders like Malaysia no longer have any projects under development, while others like Philippines and Viet Nam are moving away from new coal.

- Cambodia, Indonesia, Laos, and Thailand can follow the lead of their regional peers and commit to no new coal construction.

- Sub-Saharan Africa has a pipeline of 15GW (5% of the global total), down 47% since 2015.

- Over this period seven countries have fully scrapped their pipeline.

- This leaves 13 countries still considering coal, but with only South Africa and Zimbabwe currently constructing new plants.

- Chinese financial institutions are involved in 13 projects in eight countries, totalling 11.4GW of planned capacity (76% of the total pipeline in the region).

Following the launch of No New Coal by 2021, we are pleased to be able to share the ‘No New Coal Factbook’ produced as a collaboration between Ember, E3G and Global Energy Monitor . The ‘No New Coal Factbook’ provides individual profiles of countries that could cancel coal projects and formally commit to building no new coal power plants. This includes 40 countries that do not have any coal projects proposed together with 37 countries that have projects at varying stages of development. 16 of these countries only have one project. 24 countries were looking to receive support from China.

Through showing the collapse in the number of coal projects since 2015 our analysis highlights the growing momentum away from coal. The ‘No New Coal Factbook’ aims to inform and encourage governments to commit to no new coal ahead of COP26.

Read the No New Coal Factbook here.