If the clean economy transition in the EU is to succeed, it cannot exacerbate existing economic imbalances. Clean technology value chains can provide new opportunities for less wealthy EU member states to make the most of their assets, at the same time contributing to industrial decarbonisation. Making this work requires action at both national and EU level to remove barriers and refocus policy.

This case study looks at Portugal, which risks missing out on the global clean technology investment push. The country has strong comparative advantages in low-cost green hydrogen and the EU’s largest lithium resources. It is relatively innovative, digitally sophisticated and has a highly educated workforce. Yet, it may be leaving substantial value on the table, using its hydrogen and lithium primarily for export (for example the H2 med project) or low value-added activities.

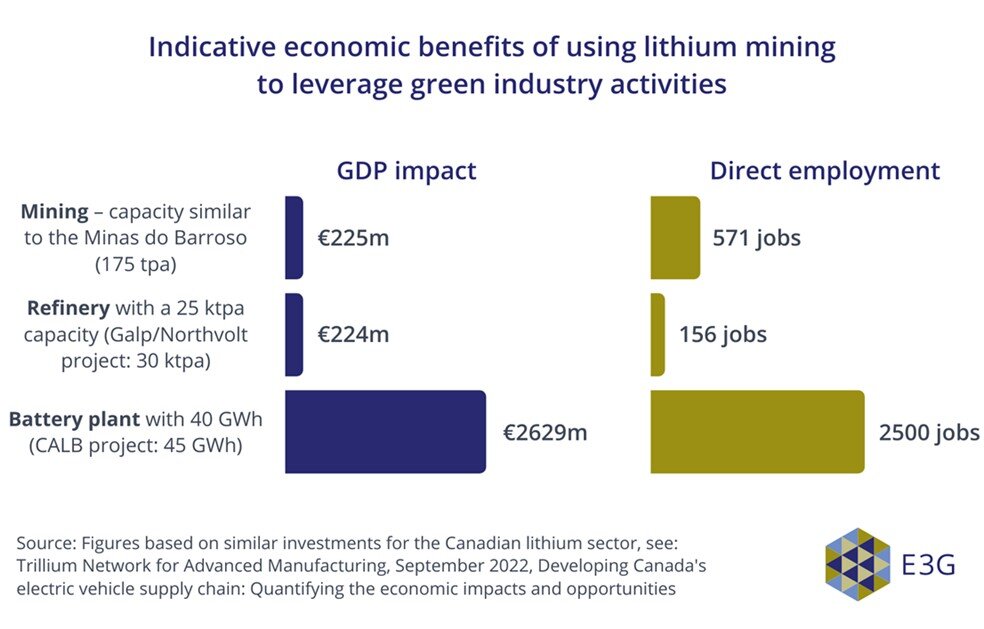

Our report finds barriers in Portugal’s political economy that prevent it seizing the opportunities that clean technology value chains offer. There is no clear strategic orientation in its industrial policy landscape, nor dedicated governance structures for clean technology value chain development. The country is struggling to scale up innovation and has few national champions to drive green industry creation. Finally, proposed lithium mining projects do not offer clear benefits to local communities.

The existing EU industrial policy framework also does not effectively incentivise clean technology value chain development across all member states. Its system based on domestic financial contributions implicitly favours wealthier countries. As a result, less wealthy member states may over the long term become exporters of key resources for the clean economy. This should be a yellow flag for the cohesiveness of the EU’s green industry transition. The EU has a choice. It can continue the status quo and exacerbate existing economic and industrial imbalances. Or, it can review its industrial policies to help achieve both cohesion and decarbonisation goals.

Recommendations

- The EU should deepen the EU Green Deal Industrial Plan funding pillar to ensure a level playing field in the financing framework. It needs to be predictable so that it supports cross-EU green industrial value chain development and gives certainty to investors.

- Portugal should refocus from its resource-level strategies and adopt an integrated value chain approach to industrial policy. This should be reflected in a green industrial strategy. There is an opportunity to set predictable local demand targets that support the development of new clean technology value chains at national level. The EU can incentivise all member states to think strategically about their comparative advantages by mandating them to develop such plans.

- Local economic value creation for lithium regions needs to be considered in the national lithium framework and when assessing strategic projects in the EU Critical Raw Materials Act.

- The EU hydrogen financing framework should incentivise priority, high value-added uses of hydrogen. It must focus on activities that can add to the member states’ industrial capacity profiles.

Read the summary for policy makers in English here.

Read the summary for policy makers in Portuguese here.