As 2025 draws to a close, Europe has clarity on the factors that limit its autonomy: structural dependencies, constrained finances, and outdated defence and industrial capabilities. 2026 will provide the EU a narrow window to move from reactive to proactive action. Progress will remain challenging in a splintered and high-stakes political landscape – one where even clear choices require bold action, the sense of urgency is mounting, and coalitions are shakier. Yet the new year also comes with opportunities to bring tangible benefits for Europe and its citizens.

For the EU, 2025 has been a year of paralysis and reactiveness to internal and external pressures – from intense deregulation pushes to trade tensions with the US and China. Its political leaders are acutely aware of how strategic vulnerabilities and dependencies across trade, supply chains, digital services, and defence leave the EU exposed to external pressures and limit its ability to act in its own interest.

The call for “Europe’s independence moment”, voiced by Commission President Ursula von der Leyen and grounded in the stark diagnosis of the Draghi Report, reflects the urgency for the EU to take charge of its own security, industrial revival and geopolitical agency. Central to this is accelerating the clean transition, which heads of state and government have confirmed as essential to Europe’s strategic autonomy, competitiveness and resilience.

Now, the EU needs to show that it can turn this diagnosis into concrete action.

The political dynamics shaping the EU’s ability to act

In 2025 we have seen the EU’s decision-making processes bend and creak under internal and external threats to its sovereignty, while it tries to tackle an ongoing competitiveness crisis. But while pressure can weaken, it can also set things in motion. Amid turbulent geopolitics, the EU could project continuity as strength, and find broader support for a more active industrial policy.

Europe’s strategic dependencies leave it exposed to foreign influence and interference, limiting its capacity to pursue its agenda in areas such as trade, technology, climate, and beyond without disruption. So far, these pressures appear successful in shaping the EU’s responses, affecting its regulatory stability.

The EU’s ability to respond to such pressures is not helped by a fragmented European Parliament. The new balance of power means two alternative majorities (EPP with groups further right, or the traditional “grand coalition” between EPP and parties to their left) are able to establish the institution’s position. At the same time, the Parliament is seen as fragmented and weakened, and often a decision-taker following the arbitrage of national governments.

2025 also marked a clear departure from Brussels’ usual process-driven approach. The European Commission has been more creative in its engagement and “pre-negotiations” with national leaders and governments, or regarding the use of consultations, impact assessments and inter-service consultations – to the dismay of the EU Ombudsman. The “college approach” has led to intense centralisation and reduced collegiality among Commissioners.

But these shifts also lead to a Europe that is able to act faster, and differently, when circumstances require. We have seen this in pictures of a selection of European leaders in the White House, EU–UK rapprochement, or coalition of the willing formations regarding Ukraine. We see increased recognition for European leaders and the role of Europe in these uncertain times. In fact, geopolitical fragmentation and uncertainty has almost reinforced the perception of the EU as a necessary anchor in times of volatility. Despite the rise of Eurosceptic sentiment, the EU’s role as a source of strength, continuity, and hope has remained resilient.

Similarly, just as the COVID pandemic helped Europe break through barriers to joint EU borrowing, the present crisis is removing hesitancy about European industrial policy. There is a growing appetite among member states to engage in more active policy to drive European reindustrialisation, including via decarbonisation. Tough questions remain over the institutional and fiscal framework to do so effectively, as well as the Made in EU / Made with EU criteria, but there is a clear direction of travel.

If this is possible, what other hesitations could be overcome in 2026?

Four tests for Europe’s independence bid in 2026

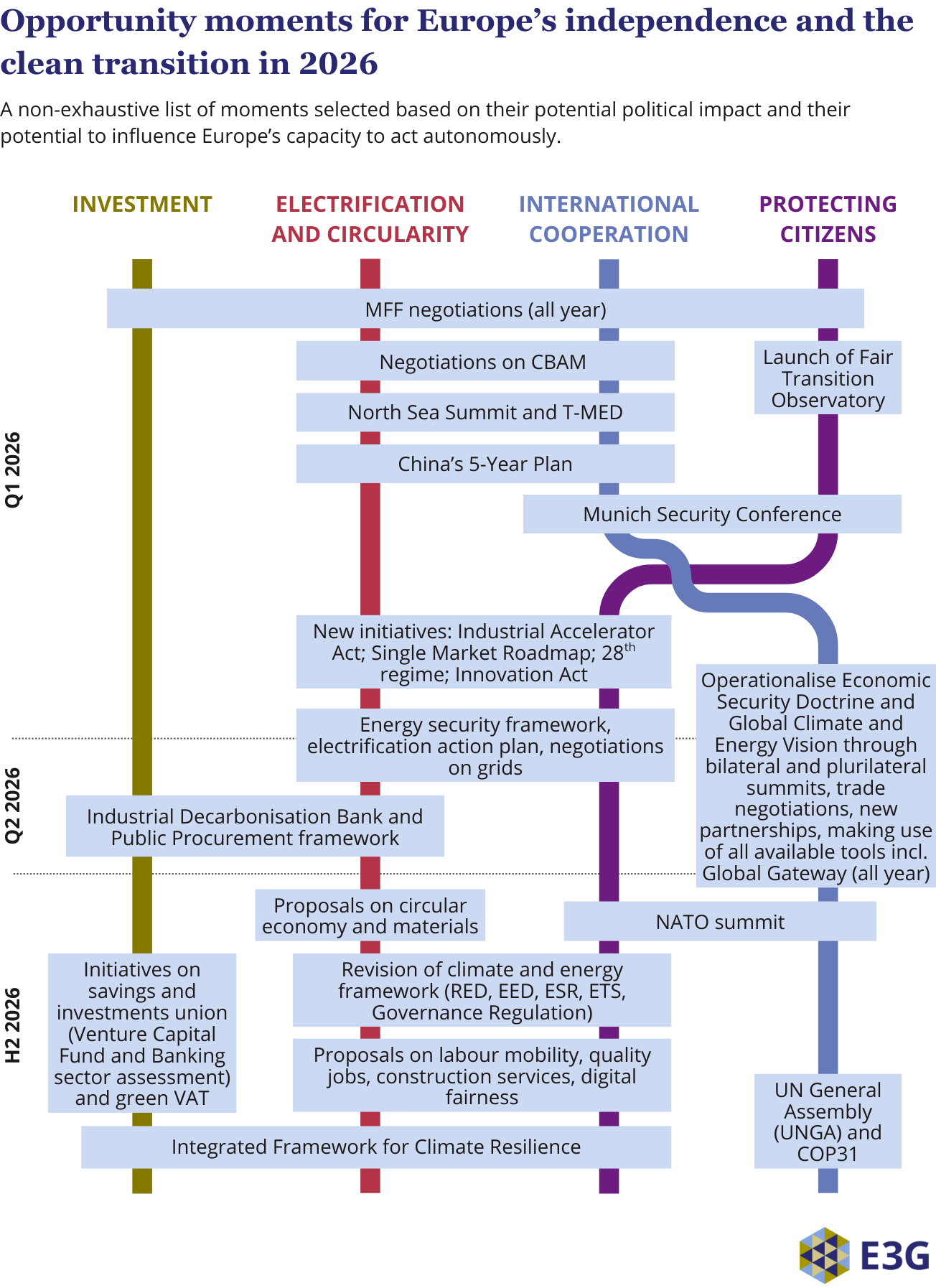

While Europe has a sharper sense of its vulnerabilities, it does not yet have a clear path to overcome them. In 2026, the EU will face four tests of its ability to become more independent.

Investment needs cut across all EU priorities underpinning the bid for greater independence. The overarching test for 2026 therefore is whether Europe can both harness upcoming openings such as the negotiations on the Multiannual Financial Framework (MFF), and create new ones, to rebuild investor confidence, strengthen Europe’s financial autonomy, and improve its capacity to mobilise public and private capital in support of its strategic ambitions.

Fiscal space is shrinking under tighter budgets, the return of stricter fiscal rules and the looming end of the post-pandemic spending boost, notwithstanding recent improvement in some economic indicators, such as modest but steady GDP growth and decreasing unemployment , or signs of global investors pivoting towards Europe. The defence, digital and clean transitions are estimated to require an additional €1,200bn per year, nearly half of which depends on public funding that existing instruments – including the proposed MFF – could not fully cover.

The “Copenhagen Declaration” revealed that major companies stand ready to invest in Europe if it accelerates the implementation of its competitiveness agenda, and the rollout of national and private-sector transition plans – if mutually aligned – is set to give investors greater clarity. Regulatory uncertainty is one factor currently dampening private investor confidence, along with geopolitical volatility and increased climate risks.

Structural issues also impede private investment. While global investors are diversifying portfolios away from the dollar, Europe still lacks a deep and liquid Eurobond market to position the euro as a reliable alternative. At the same time, there is a growing consensus that the fragmentation and limited scale of Europe’s financial system hinder the mobilisation of savings and reinforce the EU’s structural dependence on US financial markets and infrastructures.

- The MFF negotiations can anchor investment behind EU priorities – such as the clean transition, innovation and energy infrastructure – and help advance the debate on the need for stronger EU fiscal capacity and joint debt issuance. The debate on new EU own resources will resurface as a central question.

- The newly adopted 2040 climate target, the rollout of transition plans, the Industrial Decarbonisation Bank and Clean Industrial Deal measures – on lead markets, targeted EU preference and circularity – can provide clear signals to investors and improve the investability of the clean transition.

- Progress on the Savings and Investments Union – particularly reforms on pensions, financial market integration, venture capital markets and the Banking Union – can improve Europe’s financial autonomy and its capacity to mobilise savings.

- Momentum behind increased dual-use defence spending, as well as the upcoming European Integrated Framework for Climate Resilience, add further scope to align finance with security, competitiveness and resilience.

The EU’s reliance on critical imports and its exports-driven growth model are sources of vulnerability in the current global context, while a resilient domestic economy offers a lifeline on both accounts. A central test for 2026 will be whether the EU can translate its competitiveness rhetoric into an assertive focus on turning its Clean Industrial Deal into policies that effectively create lead markets for domestic clean materials and technologies.

An EU push on circular economy would significantly lower materials imports and energy use, creating new markets for affordable, European recycled materials and products. It would allow the EU to leverage Europe’s competitive edge in this area and create new business models for European innovators to scale. The direct electrification of industrial processes can decarbonise 90% of industrial energy demand, lower reliance on volatile fossil fuels, create new markets, promote technological leadership, and help businesses cut costs with modern industrial flexibility.

Electrification of industry is dependent on ramping up electrification of the energy system and upgrading grids, to resolve the long queues to secure grid capacity. This will also allow Europe to fully harness the rapid growth in renewable output, which is partly wasted through curtailment, raising electricity costs.

Electrification is also emerging as the core route to energy security and affordability, as Europe moves focus from short-term gas diversification to tackling broader structural dependencies. A shift towards a renewables-based electrified system – supported by infrastructure that is resilient to military or climate shocks, efficiency, and demand-side flexibility – is increasingly seen as the way to reduce energy costs and exposure to external shocks, and will sit at the centre of the energy debates in 2026.

- Negotiations on the Grids Package, the implementation of the Clean Energy Investment Strategy and the upcoming Electrification Action Plan can streamline grid governance and investments to align electrification needs in industry and energy systems.

- The North Sea Summit and initiatives such as the Trans Mediterranean Energy and Clean Tech Cooperation Initiative will offer openings to unlock energy security and industrial leadership benefits, and advance nearshoring of cleantech manufacturing.

- The revision of the energy and climate policy framework (CBAM, Energy Security, Governance Regulation, RED, EED, ETS) can align it with the 2040 climate target, strengthen resilience, and support a shift from gas dependency to domestic renewable electricity.

- The upcoming Industrial Accelerator Act, Circular Economy Act, Innovation Act and revised public procurement rules will be crucial to support the creation of lead markets for European clean materials and products.

- China’s 15th Five-Year Plan in March 2026 could act as a catalyst for EU policymakers, helping overcome remaining resistance to a more assertive EU-level industrial policy and focusing minds on sectors where the EU still is ahead technologically.

European officials and institutions have operated under the premise that Commission policy priorities are in the interests of the public, whether the public realises it or not. At a time where the EU is under attack from international and domestic pressures, another critical test for the EU and its member states in 2026 is whether they can develop policy that can deliver, visibly, benefits and protection for people across defence, industry, energy, investments and external action.

As Russia’s ongoing threats and the possible end of US defence commitments expose Europe’s fragility, expanding defence capabilities remains at the top of the EU’s political agenda. Nascent coalitions of the willing are emerging to overcome paralysis by consensus, and most member states are ramping up defence spending, with an emerging recognition of the importance of dual uses – for both civilian and defence purposes. Equally pertinent is shielding democracy against misinformation and foreign interference, which misleads the public against Europe’s interests and the benefits of European solutions to European problems, including the clean transition.

Competitiveness per se does not resonate with people’s everyday worries. For the EU’s strategy towards greater independence to stay politically credible, it needs to translate into energy security, affordable energy bills, attractive jobs and affordable housing. Fostering electrification, decarbonisation, circularity and clean technologies, as well as public–private concerted action in the construction and renovation sectors, holds great potential if aligned with supportive social frameworks.

More than 8 in 10 Europeans view climate change as a major problem, with increasing concerns about its impact on daily lives, notably in Southern Europe. At the same time, scientists are raising the alarm that Europe is not prepared for rapidly growing climate risks. Strengthening Europe’s resilience against climate impacts is essential to protect citizens against the increasing physical, economic and financial impacts of climate change – building confidence and a sense of safety.

- The EU’s formal push for “capability coalitions” serves as a blueprint to overcoming paralysis in other areas, while increased defence budgets – alongside the implementation of EU defence initiatives – can strengthen the dual-use of defence spending to support industry and infrastructure.

- Upcoming EU-level social policies on affordable housing, anti-poverty, labour mobility, quality jobs, fair transition and social leasing for clean products can link the clean transition to tangible improvements in living and working standards.

- Legislative initiatives on electrification, clean energy, and grid modernisation, as well continued progress on “delivery” through investment and implementation, hold potential to address people’s immediate concerns about cost and fairness, and to create space for debate about societal choices and solutions.

- The planned Climate Resilience and Risk Assessment Framework, together with the Cypriot Council Presidency’s focus on Mediterranean water resilience, opens avenues for protecting citizens against climate impacts, promoting nature-based solutions and strengthening international cooperation.

The EU’s “independence moment” faces the test of achieving greater autonomy while simultaneously expanding its global agency. It is a delicate balancing act that will require leveraging trade, investment, and diplomacy to diversify strategic partnerships and strengthen cooperation in an increasingly fragmented geopolitical and economic landscape.

There’s a growing recognition that Europe’s structural dependencies on the US, China, and Russia continue to narrow its room for manoeuvre. At the same time, rising protectionism in major economies complicates access to critical supply chains, and climate impacts in partner countries increasingly disrupt trade routes and raw-material flows.

The core challenge is to shift from a posture of risk management to one of strategic engagement. Overreacting with defensive, inward-looking measures would risk raising costs, alienating partners, and weakening Europe’s ability to shape global rules and markets for advanced technologies and clean energy. Instead, a partnering approach can enable Europe to diversify dependencies, strengthen its global influence, and position the EU as a credible partner for emerging markets and developing economies (EMDEs) pursuing their own economic transformation.

Europe will also need to maintain a strong presence at the bilateral, plurilateral and multilateral levels, where the shifting priorities of the US and others have left a vacuum. Doing so depends on a more coordinated “Team Europe” external action with greater leadership from and buy-in among member states, and ability to embed clean economy priorities across economic, diplomatic, and security portfolios.

- Growing geopolitical fragmentation creates space for the EU to present itself as a confident, reliable partner offering stability, investment, shared resilience, local value creation and transparent cooperation at a moment when many countries are reassessing their alignments.

- Operationalising the updated Economic Security Strategy can turn Europe’s risk-management narrative into a more proactive and comprehensive agenda that strengthens supply-chain resilience for the clean economy and expands the EU’s global room for manoeuvre. The Commission can accelerate its push to forge new bilateral partnerships focused on growing clean sectors and diversifying value chains through new Clean Trade and Investment Partnerships by bringing the joint economic security dimension that was missing from the recent South Africa deal. The EU can also apply this approach multilaterally, notably in the upcoming Trans-Mediterranean Energy and Clean Tech Cooperation Initiative (T-MED). This initiative is also an opportunity to showcase the unique advantages of EMDE cooperation with the EU over other increasingly engaged actors such as China and Gulf countries.

- Upcoming negotiations on CBAM, on the role of international climate credits in the EU 2040 climate target, and on the Global Europe fund as part of the next MFF are opportunities to ensure a sufficient level of EU funding is available to deliver an attractive offer to partner countries. Discussions on making Global Gateway more agile and attractive to the private sector – underpinned by the new Investment Hub – can create channels to align European industrial interests and capabilities with partner countries’ development priorities.

- At the same time, the growing weaponisation of trade and clean technology supply chains confirms that countering economic coercion by hostile states will be a key tool for reducing vulnerabilities and defending the resilience of the clean economy.

- The run-up to high-stakes bilateral and multilateral moments in 2026, including the EU–UK summit, EU–India summit, French-led G7, UNGA and COP31, provides opportunities for Europe to strategically strengthen alliances with key partners, linking objectives on climate ambition, resilience and finance with broader trade and investment goals.