On 1st July 2015 the German government agreed to introduce a new strategic reserve instead of the previously-proposed climate levy. The financial markets saw this as a successful result for the aggressive lobbying strategy of energy utility RWE, with the group’s shares seeing an immediate increase in value of 6.4%.[1] Instead of facing additional costs for its dirtiest lignite power stations, RWE will now be paid by German taxpayers to withdraw these plants from the market.

If introduced, this approach would perversely reward RWE for its past record of economic mismanagement and opposition to climate policies and energy market reforms. But the European Commission still needs to consider whether the strategic reserve is compatible with regulations that limit state aid to failing companies. The Commission must therefore scrutinise RWE’s recent actions.

The recent reality has been that RWE is losing money on many of its old and inefficient lignite plants. Despite having committed to deep cost reductions amid falling profits and massive write-downs, the company has resisted calls to close them. Our new analysis suggests that RWE has kept uneconomic lignite plants open with the intent of receiving a public bail out.

Massive losses from a high-carbon business model

RWE is losing money on many of its old and inefficient lignite plants. RWE stated in 2015 that their total conventional generation fleet was making zero cash.[2] When day-to-day capital expenditure like the costs for maintaining and upgrading equipment are included, their entire 43GW conventional generation portfolio is cash flow neutral.

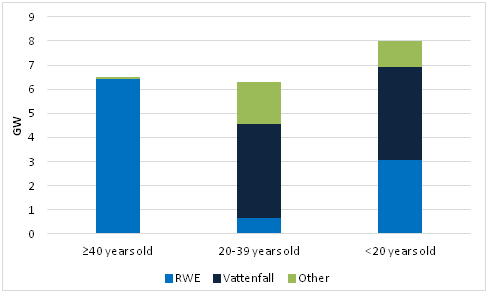

RWE’s CEO, Peter Terium, has admitted that 35 to 45% of their current conventional fleet is unprofitable.[3] Proponents of lignite power generally argue that lignite is the only profitable and secure domestic energy source that Germany has left. However, the current difficulties of RWE, which owns almost half of Germany’s lignite capacity, show that this is not automatically true. Many of RWE’s older lignite plants are likely part of this collection of plants that are operating at a loss.

RWE’s smaller lignite units are almost certainly unprofitable. Back in 2013, the CEO of RWE Generation said that their 300MW lignite units have “massive difficulties to earn their full costs.”[4] At that time, the electricity price was at €38/MWh. Today, with power prices 16% lower at €32/MWh, it is almost certain that these power stations are unprofitable. RWE currently has 11 such units, all of which are more than 40 years old.

Age of German lignite plants by owner

Source: BnetzA Kraftwerksliste

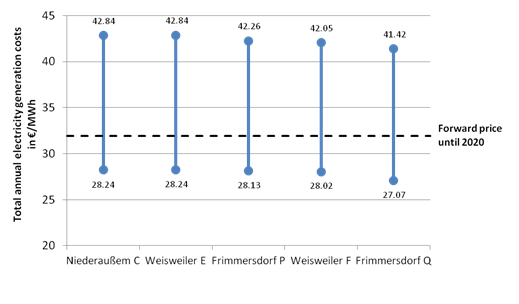

The situation seems to be particularly bad regarding RWE’s oldest units in Niederaußem, Weisweiler and Frimmersdorf. In May 2015, RWE (alongside MIBRAG and Vattenfall) disclosed their cost structure to investment bank Lazard. Lazard subsequently aggregated and published the data providing an insight into the profitability of these companies’ lignite.[5] E3G estimates that the electricity generation costs at these three power stations lie in the range of €27 to €43/MWh (see Figure 3). Compared to current and forward electricity prices of €32/MWh it is highly questionable whether these units are profitable. The difference between the lower and upper estimates is "fixed fuel and mining costs". These relate to costs such as machinery and land purchasing. In the short-term, many of these costs may not be avoidable. However, in the medium-term, most of them should be avoidable – not least because closing the oldest units will leave more lignite for the remaining units, making further expansion of mines unnecessary. Vattenfall has already recognised this, and stopped future expansion of mines. Since this data was published as late as May 2015 it can be assumed that it already includes the extensive cost-cutting measures that RWE has conducted over the last few years. This leaves little ambiguity that – if these units are not unprofitable – they are at best operating at the margin of profitability.

Profitability of RWE’s oldest lignite units

Source: E3G estimate

RWE outage data furthermore reveal that 4 of RWE’s most inefficient lignite units are each having major outages this year, lasting at least 5 weeks.[6] Regular outages are mandated for maintenance reasons. Extraordinarily long outages like in this case imply that a lot of maintenance work with high capital expenditure is necessary to retain the operating permit.

All this is despite RWE announcing, back in 2013, that it would undertake “selective capex” after suffering the worst operating results in the company’s history.[7] Selective capital expenditure implies that units not justifying capital expenditure would be closed. The company has indeed enacted stringent cost-cutting measures. However, its old lignite plants seem to be exempt. As part of the cuts, RWE is currently looking to close over 8GW of capacity until 2016.[8] Yet only 150MW of this comes from lignite, from the company’s two smallest units at the Goldenberg power station. At the same time, RWE has shut down over 3.7GW of much less polluting gas stations.

Keeping lignite open, aiming for a bailout

RWE has continually sought to keep old lignite stations open over the past few years. From a normal business perspective, it is surprising that RWE has not already decided to close these old lignite power stations – especially since the market outlook for lignite in Europe and Germany is only set to become worse. This approach can therefore be interpreted as a deliberate attempt to force the hand of policy-makers.

Right now, it appears that this strategy has partially paid off. According to an agreement by the government coalition on 1 July, Germany is now going to introduce a 2.7GW capacity reserve where lignite plants will essentially receive subsidies for going on standby. This measure replaces the climate levy, a much more ambitious proposal which would have fined the operators of inefficient lignite stations for polluting beyond certain emissions thresholds.

It would appear that RWE has taken a bet on being too big to fail, by keeping old lignite plants open long past their economic due date, trusting that the government would be willing to bail them out with a capacity mechanism if necessary. This might have seemed like a safe bet. After all, RWE has systemic importance in certain regions of Germany. Particularly in North-Rhine Westphalia, suppliers and jobs, but also municipalities owning shares in RWE, depend on its lignite mines and power stations. This enabled RWE to run a frontal assault on the climate levy, together with the energy and energy-intensives union (IG BCE) and local politicians in affected regions.

The new measure will now lighten the emissions reduction burden for the power sector while shifting the costs from the utilities to the taxpayers. RWE is set to be the single largest beneficiary of the reserve. According to DIW, old RWE lignite plants will likely account for roughly 1.5 GW of the 2.7 GW reserve.[9] According to Energy Minister Gabriel, the level of capacity payments will be €230m per year.[10] If this money is allocated proportional to the capacity provided, this would mean that RWE could receive about €130m per year from German taxpayers. This is not peanuts for the company – it amounts to 13% of the 2014 operating result from its entire conventional generation business.[11] But this is significantly less than RWE was hoping for.

Not yet over the line: state aids still in play

Across Europe, a number of utilities have complained about lost profits, which have principally resulted from a combination of the economic crisis, structural overcapacity and their own incompetence. RWE has notably been at the forefront of these calls for support, which have typically claimed that there is a need for governments to act to ensure that “the lights stay on.” Capacity mechanisms have therefore emerged as a convenient fig leaf that disguises recompense to generators as a means of addressing security of supply concerns. The European Commission has however rightly warned of the negative impacts such measures would have on the Internal Energy Market, and has set out guidance that would limit negative impacts.

More recently, in April 2015, the European Commission announced a sectoral investigation into proposed capacity markets spanning 11 EU member states.[12] With increased regional cooperation on electricity transmission and interconnection, the Commission is keen to ensure that national capacity measures do not distort market signals, and are compatible with EU decarbonisation objectives. This investigation already includes Germany, so the proposed new strategic reserve is already slated for review. This was acknowledged by the German government in its announcement on the new agreement, stating that it is committed to “clarifying compatibility with EU state aid regulations with the EU Commission”.[13]

As the guardian of Europe’s internal market, the European Commission does not only have to consider Germany’s policy proposals but also take into account RWE’s approach over recent years. For, as the Commission itself states:

“In liberalised markets, investments are not guaranteed by the State. Only where there is a real threat to generation adequacy and security of supply as a result of closure or mothballing does the financial viability of existing plants become a matter of public concern. It is very important that there should not be state support to compensate operators for lost income or bad investment decisions.” [14]

Based on the currently available evidence it appears that the strategic reserve is principally a means of bailing out RWE’s business model, with the lifetime of old lignite plants deliberately lengthened in an attempt to secure financial support. It isn’t the fault of taxpayers and consumers that RWE pursued a high-carbon strategy and then dug its heels in to defend it. This is a bad use of public money. RWE shouldn’t celebrate too soon.

You can read this post in German here

References

[1] https://www.bloomberg.com/news/articles/2015-07-02/germany-to-close-coal-plants-in-effort-to-curb-pollution

[2] See slide 8 of the RWE presentation “Paving the way for growth with continued focus on financial discipline”. The conventional fleet includes fossil fuel as well as nuclear power plants.

[3] https://www.wsj.com/articles/rwe-plans-further-cost-cuts-1425968788

[4] https://www.ingenieur.de/Branchen/Energiewirtschaft/Unrentabel-RWE-ueberprueft-Kraftwerk

[5] Lazard (2015) Potentielle Auswirkungen des “Nationalen Klimaschutzbeitrags” auf die Braunkohlewirtschaft

[6] Gathered from outage data published by RWE

[7] See slide 12 of their presentation “3 steps to long term value”

[8] See slide 9 of the RWE presentation “Paving the way for growth with continued focus on financial discipline”.

[9] https://www.claudiakemfert.de/fileadmin/user_upload/Inserts/Kurzbewertung_des_neuesten_Kompromissvorschlags.pdf

[10] https://www.wwf.de/fileadmin/fm-wwf/Publikationen-PDF/WWF-Stellungsnahme-Ein-neues-Klimaschutzinstrument-fuer-den-Stromsektor.pdf

[11] This is before day-to-day expenditure, taxes, etc. are subtracted.

[12] https://uk.reuters.com/article/2015/04/29/uk-eu-energy-competition-idUKKBN0NK0YV20150429

[13] Eckpunkte für eine erfolgreiche Umsetzung der Energiewende- Politische Vereinbarungen der Parteivorsitzenden von CDU, CSU und SPD vom 1. Juli 2015

[14] European Commission, 2013. SWD(2013) 438 final, p10

This project action has received funding from the European Commission through a LIFE grant. The content of this section reflects only the author's view. The Commission is not responsible for any use that may be made of the information it contains.