A significant quantity of gas infrastructure is being planned in Europe, with security of supply often quoted as a key driver for new infrastructure.

This infrastructure expansion comes despite recent reductions in EU gas consumption. Meeting EU energy and climate targets will require a reduction in fossil fuel use over time, raising questions about how new gas infrastructure is planned and prioritised in the energy transition. This new report from E3G explores Europe's options.

A smarter approach to energy security can deliver security for lower cost

Energy security is too important for Europe’s future to be managed within narrow silos. This report addresses how a more integrated approach to energy security can help Europe stay secure for lower cost, by:

- Treating energy efficiency as a deployable infrastructure

- Maximising the synergies between different infrastructure types

- Ensuring consistency with EU climate and energy goals, rather than pursuing contradictory policies.

Current approaches lack alignment

If current plans were to materialise, the EU would see a significant increase in gas infrastructure, with pipelines and LNG terminals under development collectively representing a 58% increase in EU gas import capacity.

Figure 1: Projects representing a 58% increase in EU gas import capacity are under development (Source: E3G, Bruegel, ENTSOG, European Commission)

This new infrastructure is planned based on the expectation of rising gas demand. There are uncertainties about whether this will materialize. EU infrastructure planners and institutions have a track record of persistently overestimating gas demand. Despite previous expectations of a significant increase in gas consumption, EU gas demand has fallen by a fifth since 2010.

Looking forward, projections diverge. Demand falls significantly in scenarios in which EU energy and climate targets are met, but rises in scenarios where this constraint is not present. Projections of gas imports follow a similar trend. The primary EU gas network development plan is not, however, based on meeting EU energy and climate targets. As a result, the gas demand assumed for network planning is 30-55% higher in 2030 than a scenario in which the proposed 30% energy efficiency target for 2030 is met – creating the risk of policy misalignment.

Gas infrastructure also continues to be planned largely separately from electricity and demand-side infrastructure, despite the interactions between different sectors. This means opportunities to make use of electricity infrastructure and demand-side investment for increasing security of gas supply may be missed.

Infrastructure needs are limited and can be lowered further

To assess the potential of a more integrated approach to energy security, energy consultants Artelys and Climact were commissioned by E3G and partner organisations in the Energy Union Choices consortium to model different infrastructure strategies against a range of demand scenarios and potential shocks and disruptions. The results are striking:

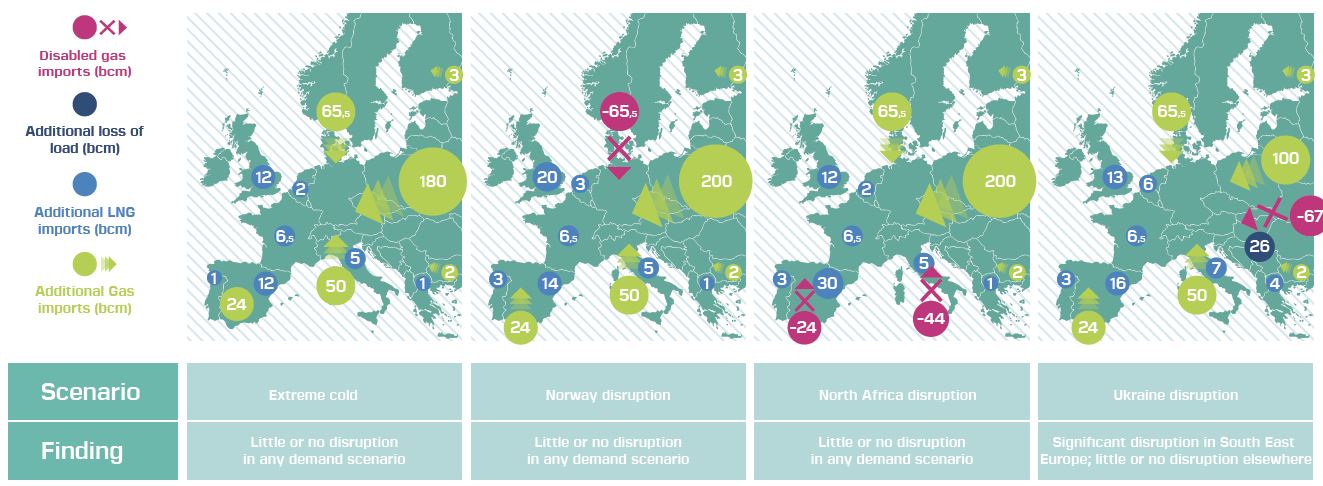

> Europe’s current gas infrastructure is highly resilient to supply shocks; limited investment may be needed in South East Europe

A range of demand scenarios and extreme disruption cases were tested – including an extreme cold year and year-long disruptions to Norwegian, North African and Ukrainian imports. Existing EU gas infrastructure was sufficient to ensure physical security of supply in nearly all of these cases. The exception to this is South East Europe, where steps need to be taken to ensure physical security of supply in the event of a disruption from Ukraine.

Figure 2: Europe’s existing gas infrastructure provides resilience against a range of shocks and demand scenarios; investment may be needed in South East Europe (Source: Artelys / Climact)

> Integrating gas and electricity systems delivers supply security at lower cost

A smarter integration of European gas and electricity systems and demand-side management can significantly decrease investments in gas infrastructure. In both the ‘high demand’ and the ‘current trends’ scenarios, investment needs are cut in half by utilising the flexibilities of cross-border electricity network to help manage the impacts from a disruption to gas supplies.

Figure 3: An integrated perspective looking at gas, electricity and buildings efficiency together has the potential to reduce gas infrastructure investments by 80% (Costs of gas infrastructure to ensure security of supply, in billion € (Source: Artelys/Climact)

> Demand reduction and buildings efficiency significantly reduces investment needs

Buildings are an integral part of the EU’s energy system. Implementing demand side measures in line with a 2030 efficiency target can reduce infrastructure investment requirements by up to 74%. An integrated perspective looking at gas, electricity and buildings efficiency together has the potential to reduce gas infrastructure investments by 80%.

> Delivering the EU’s 2030 targets can significantly reduce gas imports into Europe

A low carbon pathway in line with its 2030 climate and energy targets can reduce imports by 95bcm (-29%) compared to a scenario that fails to meet these targets.

> New gas infrastructure assets will be superfluous by 2050

Once built, new gas infrastructure has a lifetime of 40 years or more. By 2050, the dual impact of economy-wide efficiency improvements and electrification trends will sharply reduce gas demand in Europe – making new gas infrastructure superfluous before the end of its economic life.

New approaches are required

A smarter approach to gas security is needed. It should:

1. Treat energy efficiency as infrastructure

The first best option for managing energy security risk is effective management of energy demand. Meeting the 30% energy efficiency target for 2030 at European level makes the security challenge manageable. Demand-side investments should be given parity with other forms of infrastructure for energy security and be treated as a deployable option rather than as a fixed externality. Proposed new gas investments should also be tested against alternatives – including demand reduction, demand response, and electrification.

2. Plan for the future we’re aiming for

Network developers should base gas and electricity infrastructure planning and prioritisation on scenarios that meet EU climate and energy targets, rather than undermining them.

3. Integrate infrastructure planning

Independent, integrated and transparent assessment of security of supply is needed to ensure proposed gas infrastructure is fully in the interests of consumers.

4. Prioritise software over hardware

Security depends more on system rules more than on new pipelines. The EU should continue to implement market reforms and crisis response provisions.

5. Test projects for long-term viability

Lock-in and stranded asset risks change the economics of new gas infrastructure. Projects should be tested for viability in a low carbon future.

6. Phase out public funding

There are better uses of public money than large-scale investment in new gas infrastructure that may not be needed. EU funding for new gas infrastructure should be phased out by the time of the next European budget.