Sustainable infrastructure investment is essential to achieving the UN’s Sustainable Development Goals and the Paris Agreement on climate change, as it underpins the achievement of sustainable inclusive growth.

The New Climate Economy report estimates that the world is expected to invest around USD90 trillion in infrastructure over the next 15 years, more than the value of the world’s existing stock, and that the investment choices we make over the next 2-3 years will either start to lock in a climate-smart inclusive growth pathway, or a high-carbon, inefficient and unsustainable pathway.

Multilateral Development Banks (MDBs) are in a unique catalytic position. Given the fiscal constraints faced by many government's, they are key in complementing governments limited resources and scaling up investment. They play a role in both construction and operational stages of infrastructure development – both providing finance but also the technical expertise necessary to support strategy development, investment planning and project preparation.

Indeed, MDBs have already made pledges to scale up their infrastructure investment, and are part of many different initiatives. Of the sustainable infrastructure initiatives identified by Mercer last year, four of them had at least four of the MDBs as members. The Public-Private Infrastructure Advisory Forum (PPIAF) aims to enable the environment focusing on reducing regulatory and policy risk for infrastructure private investment; SOURCE provides the public sector with an infrastructure project preparation tool; the Global Infrastructure Facility (GIF) brings together private and public stakeholders to draw on their expertise to deliver complex public-private infrastructure projects; and the Sustainable Development Investment Partnership aims to address the mismatch between investor needs and project funding requirements through blended finance. There are also more specific initiatives associated with implementation of the Paris climate goals, such as NDC Invest from the Inter-American Development Bank (IADB).

Despite this, a preliminary assessment of MDB investment data shows that MDBs are struggling to redirect their finance activities to become sustainable.

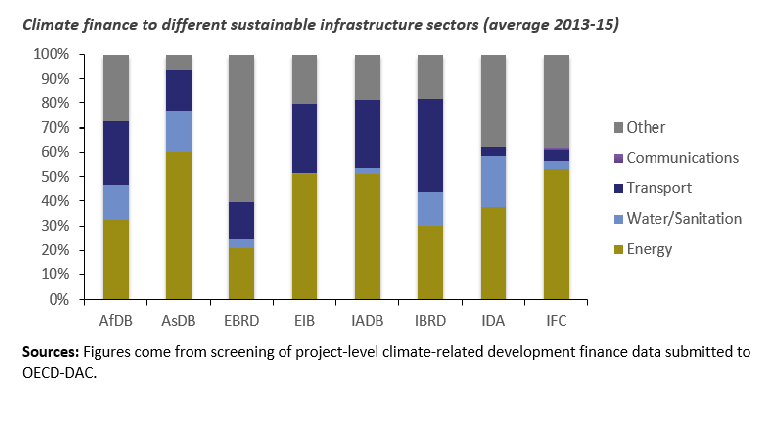

In the Organisation for Economic Co-operation and Development (OECD) reporting system, “infrastructure” refers to the sectors of water and sanitation, energy generation and support, transport and communications. E3G has analysed the most recent (2015) comprehensive project-level data reported by these banks to the OECD. We found that of these infrastructure sectors, most went to energy projects, followed by transport, water and communications projects. We have compared this data with the total spending by each bank in these sectors. The main focus is on transport, water and energy since only very small amounts of climate finance are currently being allocated to communications.

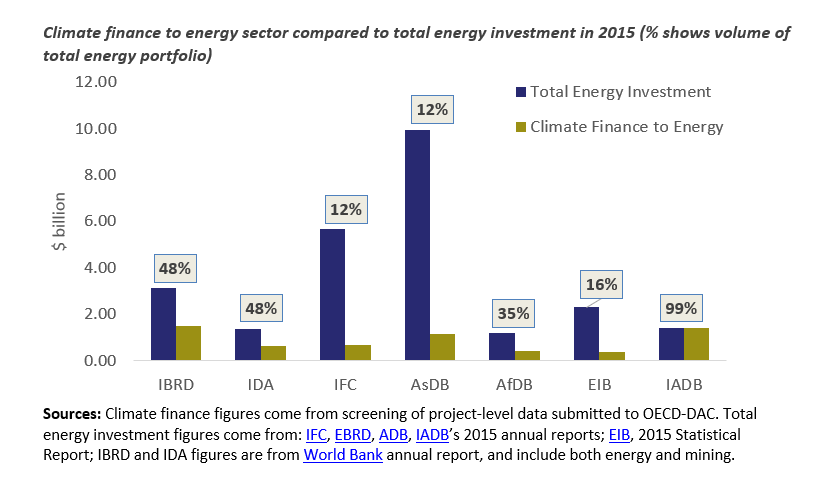

What progress on scaling up climate finance in the energy sector?

The data indicates that for the Inter-American Development Bank (IADB) in 2015, almost all energy spending was clean. Less progress has been made in the Asian Development Bank (ADB) and International Finance Corporation (IFC): here only 12% of the energy portfolio is clean energy, meaning very mixed signals are being sent to the market and client countries. A similar analysis was not possible for the European Bank for Reconstruction and Development (EBRD) due to reporting discrepancies. This demonstrates the need for transparency and consistent reporting on climate finance.

Missing opportunities in transport and water

In the transport sector, our analysis appeared to show nearly all MDBs could make much more progress in scaling up finance for low-carbon and resilient transport.In particular, the IFC did not appear to direct any climate finance towards the clean transport sector despite high levels of investment in this sector (e.g. USD 3.4 billion invested in transport and logistics in 2015 alone). The International Development Association of the World Bank also appeared to have only minimum amounts of climate finance allocated to transport. Interestingly, the EBRD, EIB and IADB all had low levels of climate finance being allocated to water and sanitation during this same period.

These gaps could demonstrate opportunities for the multilateral development banks to build coherency in their portfolios and scale up investment in sustainable infrastructure, helping to achieve their climate finance goals.

Need for a shift from an incremental to integrated approach

One of the challenges with the ‘climate finance’ pledges by the development banks is the banks may have an incentive to inflate their figures, for example by adding on a ‘resilience component’ of a conventional road project, and then claiming this is now a climate-related project.

We argue a shift in thinking is now needed. Sustainability should not be an ‘add on’ but rather needs to be integrated into all planning decisions on infrastructure at an early stage. Achieving the goal of keeping global warming below 2 degrees centigrade requires fundamental re-engineering of the global economy, with a focus on quickly shifting away from fossil fuels, for example by introducing electric cars, better public transportation, and sustainable agriculture.

To make the required transition to a low-carbon economy, MDBs cannot just apply incremental changes to projects. Instead, transformative changes need to be integrated into how MDBs undertake their financing and advisory activities. The MDBs are key in financing infrastructure in the global south, where approximately 60% of infrastructure investment is needed (USD 54 trillion). Thus it is important that they re-orientate their activities towards sustainable and resilient infrastructure. Moreover, MDBs are key in ensuring the next generation of infrastructure doesn’t suffer from the same failings as existing projects. For example, in the energy sector the focus shouldn’t be exclusively on providing new sources of supply but instead finding new ways of managing energy demand. Therefore, energy efficiency should be a core part of energy infrastructure.

We must reinterpret what we traditionally think of as infrastructure to reflect changing technology, business models and consumer demands. It means including energy efficiency, in buildings; EV charging facilities; and other 21st century infrastructure.

Furthermore, it will be important to recognise reducing emissions and promoting resilience to climate impacts are two sides of the same coin. If only one of these aims is focused on, it could create perverse incentives – for example, investing in energy efficiency to extend the lifetime of coal plants. Or upgrading fossil fuel infrastructure so it is resilient to climate impacts, such as ports which are exporting coal.

Sustainable infrastructure should not just be about labelling projects as ‘green’ or putting in safeguards at a late stage of project development. It needs to be built in right from the start of project planning and selection. Fortunately, this upstream end of project planning is where the MDBs are often acting e.g. with initiatives such as NDC Invest, development policy lending, and country partnerships. As such, the development banks are well positioned to think about this.