More than seven years on from the financial crisis, Europe still faces a range of threats including high unemployment, social inequality and high levels of public debt. Questions are being asked about whether Europe will still be able to shape economic, social and environmental standards for the rest of the world and whether and when its economy will finally recover. Continued low levels of investment in the European Union (EU) have limited employment opportunities and the scope for sustainable development. In turn, this has led to a weakening of social cohesion and investor confidence, with the knock-on effect that the EU now faces a pension fund deficit estimated at €428bn.

Facing these issues head on and placing the need to respond to Europe’s social but also environmental problems at the heart of the economic solutions proposed will be important for success. It is by identifying responses to Europe’s social and environmental problems that the European Commission can do most to reverse the EU’s fortunes.

Recognising this, the European Commission has announced two new proposals. First, to double the financial capacity and duration of the European Fund for Strategic Investment (EFSI) to provide at least €500 billion of investments by 2020: of which at least 40% will be dedicated to climate action. Second, it announced a Capital Market Union (CMU) refresh – including the establishment of an expert group to develop a comprehensive strategy on sustainable finance. This is welcome.

This report outlines a ‘Sustainable Finance Plan 2030’ that focuses on three key aims and objectives that should be central to the Commission’s strategy on sustainable finance. First, the Commission should focus on increasing investment in sustainable infrastructure. It should use the current infrastructure investment gap as an opportunity to boost development and employment opportunities, shore up investor confidence in the European project, and put the EU on a pathway to sustained economic recovery whilst managing climate risk. Second, it should look for opportunities to increase responsible investment practices. The need to address social and environmental problems should be at the heart of the financial reform agenda to enable sustainable growth. Third, the Commission should improve climate risk disclosures. Good governance and better information can help improve corporate accountability, an enabler of inclusive prosperity. Eight priority actions are recommended to take this forward.

Sustainable Infrastructure

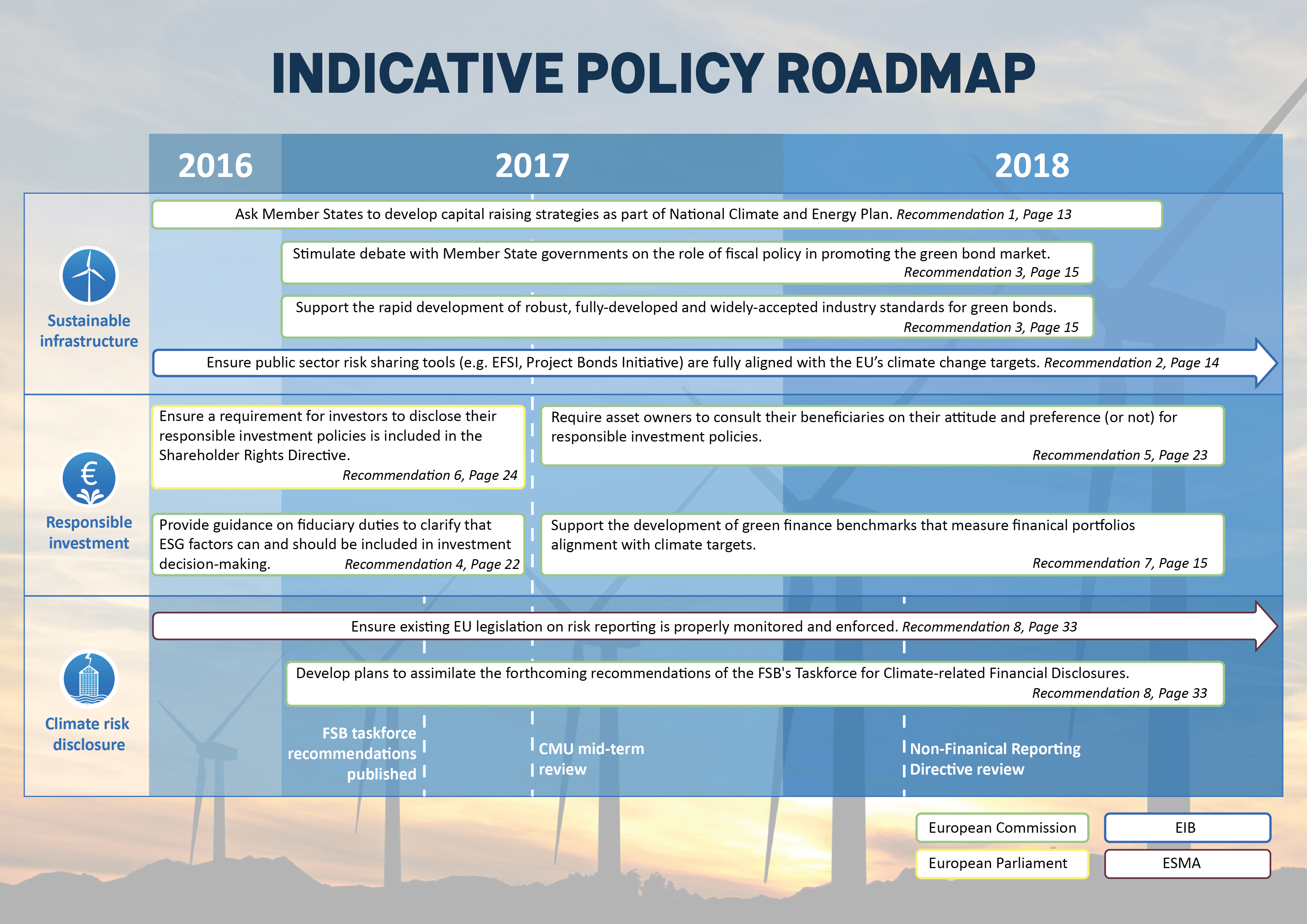

- Recommendation 1: The Sustainable Finance Plan 2030 should explicitly link the CMU and Investment Plan to the Energy Union, by asking Member States to develop National Capital Raising Plans as part of their National Energy and Climate Plans (NECPs). This would make sustainable investment opportunities more visible to the private sector and increase investor confidence in the NECPs.

- Recommendation 2: To effectively crowd in private capital, the Sustainable Finance Plan 2030 should ensure that all European financial public sector risk-sharing tools (e.g. the EFSI and Project Bonds Initiative but also grants and financial instruments developed under the wider Multiannual-Financial Framework) are fully aligned with the EU’s climate targets.

- Recommendation 3: The European Commission should support the rapid development of robust, fully developed and widely accepted industry standards for green bonds. Following that it should use its convening power to stimulate debate with Member State governments on the role of fiscal policy in promoting the green bond market.

Responsible Investment

- Recommendation 4: The European Commission should end the debate on environmental, social and governance (ESG) risk in the context of fiduciary dut y as soon as possible. It should provide guidance to the competent Member State authorities on how they should interpret fiduciary duty in the national legal context. This guidance shou ld clarify that asset owners have a duty to pay attention to long term factors including ESG factors where they are likely to be financially material. Authorities should also clarify that assets owners and managers are permitted, and indeed encouraged, to take other ESG issues link ed to beneficiaries’ quality of life or ethical views into account if doing so would not pose a risk of material financial detriment to investments.

- Recommendation 5: The European Commission should develop legislative proposals to require asset owners to consult their beneficiaries on their att itude to and preference (or not) for having their money invested sustainably. Such a proposal would improve accountability in the investment system and build trust in financial services as a force for good.

- Recommendation 6: The European Commission should improve transparency around responsible investment by proposing mandatory requirements for all asset owners to disclose information about their responsible investment policies and the implementation of those policies. This should result in the asset owners’ service providers (asset managers, investment consultants etc.) providing the information and advice their clients need, for example so-called non-financial performance factors, engagement activities (including voting decisions) and their overall impact.

- Recommendation 7: The European Commission should support the development of green finance benchmarks that measure portfolio alignment with climate targets. It should then recommend that Member State prudential regulators adopt regulat ion that asks financial institutions to disclose whether their activities align with scenarios that keep global temperature increases to below 2°C and also 1.5°C using these b enchmarks.

Climate Risk Disclosure

- Recommendation 8: The European Commission should incorporate into the mandate of the new expert group on sustainable finance an early focus on ho w recommendations from the Financial Stability Board’s Task Force on Climate-related Financial Disclosures can be best assimilated into the EU’s existing reporting framework. It should also consider two other issues: through what means decision-useful reporting can be best enforced to enable regulators at a national and EU level to fully understand the financial systems’ exposure to climate risk; and the need to move beyond reporting of risk to how companies intend to take action and report on efforts to mitigate those risks.

Read the full report A Sustainable Finance Plan for the EU [PDF 4Mb]