The central paradox of today’s energy system is that even with abundant supply, energy security is not guaranteed. Importers accounting for over two-thirds of seaborne oil and gas demand are dependent on supplies transiting a small number of maritime and domestic chokepoints. These chokepoints pose an unavoidable, systemic risk of disruptions to transits, which cause price shocks, insurance withdrawal and physical supply constraints that cascade rapidly across the system. The most durable route to resilience for importers is to reduce dependence on oil and LNG through electrification, efficiency, grids, storage and domestic clean energy.

No importer is insulated from chokepoint risks

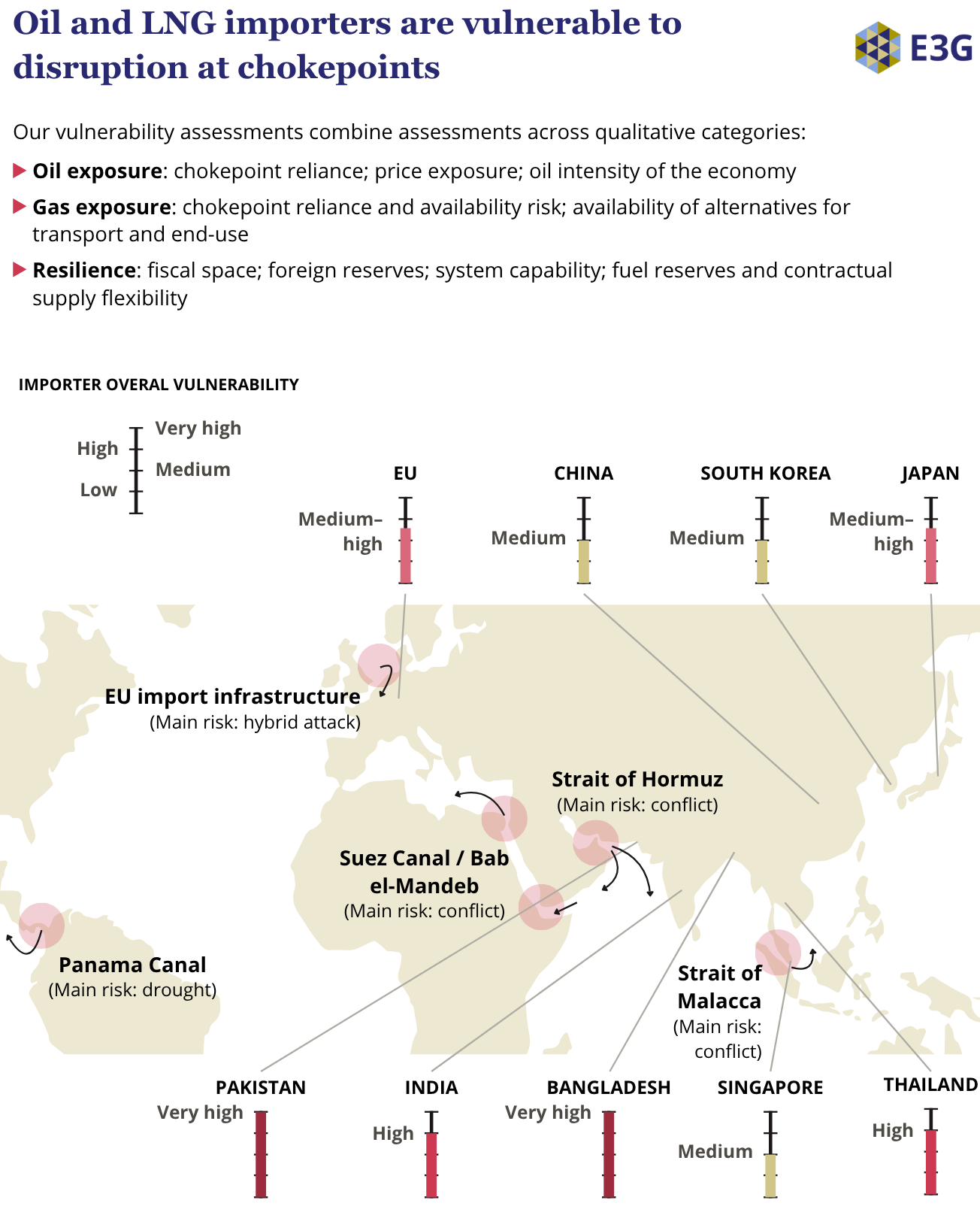

Global price transmission binds all importers into system vulnerability. However, the risk is not equally distributed. Vulnerability depends on a country’s level of exposure and resilience against chokepoint shocks.

In our report, Beyond Securing Supply: Chokepoint risk for oil and gas importers, we assess what this systemic risk means for nine major importers. Our assessments take into account four maritime chokepoints and one domestic in the form of the EU’s import infrastructure.

The current energy system is particularly vulnerable to chokepoint risks

Oil and gas transports are exposed to continuous and immediate risks. Disruptions can affect prices and availability within days, and spread quickly through the economy because oil and gas are core inputs to transport, electricity and industry. This affects inflation, trade balances, fiscal spending and economic growth simultaneously.

These risks arise not just due to physical disruptions, but also “paper chokepoints”: insurance withdrawal, sanctions, inflexible contracts and freight constraints. Increasingly, climate impacts compound the risk, through for example droughts in the Panama Canal, and extreme weather hitting ports and other infrastructure.

While fossil fuel supplier diversification can provide short-term relief from disruptions, it risks locking in structural exposure to chokepoint risks. Clean energy provides the more durable route to energy security in the long term, by displacing future oil and gas imports.

Like all seaborne commodities, clean energy supply chains also face chokepoint risks, but they are different. Disruptions slow future deployment rather than cutting current supply. The macroeconomic effects are slower and more indirect, giving governments and suppliers time to respond. The risk posed by geographic concentration of critical minerals and manufacturing can be managed through stockpiling, substitution, recycling and shipping flexibly.

Recommendations to oil and gas importers

- Deploy immediate crisis stabilisation: Coordinate oil and gas stock releases; implement emergency demand cuts; fast-track grid connections for new renewable generation.

- Fast-track short-term measures: Use supplier diversification as a short-term bridge, but avoid new long-term contracts: these lock in chokepoint risk for a generation.

- Reduce long-term structural exposure to chokepoints: Reduce demand for oil and gas through clean energy rollout and energy efficiency measures, which provide long-lived, locally generated resilience.

- Use defence capabilities to buy time, but accept they do not boost resilience: Military operations can limit short-term disruptions, but they are costly and resource intensive.

- Strengthen energy systems resilience: Future-proof clean energy by diversifying critical mineral and cleantech supply chains; boost cyber and subsea security.

Download the report: Beyond Securing Supply: Chokepoint risks for oil and gas importers

Download the executive summary

Supplementary data

Full data sets are available, underpinning findings presented in the report:

* Estimates of importer exposure to maritime chokepoints.

* Assessments of importers’ structural vulnerability to chokepoint risk.