Setting out its net-zero emissions pathway today, the International Energy Agency has ended any suggestion gas could be considered a “transition fuel”, with big consequences for industry and geopolitics, writes Jonathan Gaventa, an E3G energy policy consultant.

The idea of gas as a ‘transition fuel’ was killed off today by the International Energy Agency (IEA) with its net-zero emissions pathway. The report sets out the radical reductions in fossil fuels, including gas, required to reach the Paris Agreement aim of limiting global warming to below 1.5°C. Natural gas use peaks slightly later and falls more slowly than coal or oil in the pathway, but its decline is clear, representing a major reversal for the natural gas sector. This shift will have far-reaching consequences for the operation of energy systems and for global financial flows and geopolitics.

Natural gas is responsible for 21% of energy-related CO2 emissions and is the world’s fastest-growing fossil fuel. While coal emissions have plateaued and oil emissions have slowed, emissions from natural gas are expanding at an average rate of 3% a year. Methane emissions associated with gas production compound the climate problem for natural gas even further.

The IEA’s net-zero pathway represents a striking new future for natural gas and the wider global energy system.

IEA scenarios are highly influential in shaping energy investment strategies and government policies, and used as a reference for future energy trends. This report could have particular influence as the first scenario that explicitly meets the aims of the Paris Agreement, limiting cumulative CO2 emissions to within the carbon budget assessed by the Inter-governmental Panel on Climate Change (IPCC).

Since the Paris Agreement was signed, countries representing 70% of emissions have committed to net zero or 1.5°C goals, together with hundreds of cities, companies and investors. The IEA report will give them clear guidance on what a 1.5°C-compatible net-zero pathway looks like, and help shape policy and investment decisions.

Net-zero milestones

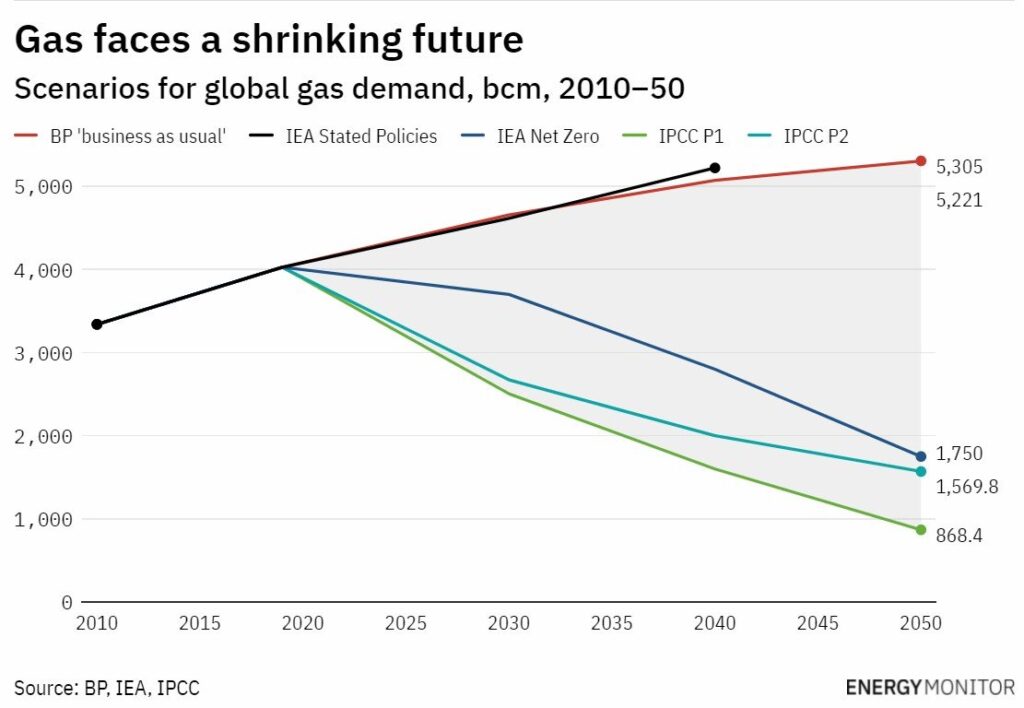

In headline terms, gas demand rises through the 2020s in the net-zero pathway before shrinking to 8% below 2019 levels by 2030. This may seem like a small contraction, but it contrasts sharply with the IEA’s previous ‘stated policies’ scenario, which saw gas consumption grow by 15% by 2030 compared with current levels. In short, in nine years, the global gas market could be a nearly a fifth smaller than what industry is expecting.

In the net-zero pathway, by 2050 gas consumption is 55% lower than today. This drop represents an enormous turnaround from industry’s trajectory and current growth patterns. The BP Energy Outlook foresees a 38% rise in gas use by 2050 in its ‘business-as-usual’ scenario, suggesting the global gas market in 2050 will be two-thirds smaller in a net-zero pathway than under today’s trends.

Sectoral milestones in the report bring this new direction sharply into focus.

Across the economy, the world reaches net-zero emissions from energy by 2050. Industrialised countries need to reach this milestone by around 2045, and swiftly move to net-negative emissions. Any remaining fossil gas use will either be for non-combustion purposes, such as the production of fertilisers, coupled with carbon capture and storage (CCS), or linked with negative emissions.

In the net-zero pathway, no new oil and gas fields are approved for development beyond projects already committed as of 2021 – and “some fields may be closed prematurely”. Even oil majors that claim to have net-zero targets (such as Total or Shell) are still planning to continue exploration and expand gas production for the next decade, and dozens of major gas export projects are in the development pipeline across the world. None of these mega-projects are needed in a net-zero pathway, and will end up stranded unless they push more expensive sources of gas off the system.

At the same time, methane emissions from fossil fuels are reduced by 75% by 2030 thanks to better detection methods and changing industry practices. As well as producing less than previously planned, the gas industry will need to become more efficient and accountable in the next nine years.

In the power sector, advanced economies reach overall net-zero emissions electricity systems by 2035. The rest of the world is not far behind: net-zero emissions in electricity is achieved globally by 2040. By 2050, more than 90% of power generation comes from renewables, with nuclear representing most of the rest. Implementing this goal means a massive scale-up of wind and solar power generation capacity – 20-fold for solar and 11-fold for wind by 2050 – and quadrupling investments in power transmission and distribution infrastructure.

These milestones suggest there is no time left for a ‘gas bridge’ in the power sector, either in advanced or emerging economies. Gas power plants typically have an economic lifetime of 20–30 years, which means anything built today will still be operating after 2040 when global electricity systems should be fully decarbonised.

Governments and utilities in advanced economies will need to accelerate plans to replace existing unabated gas generation and repurpose or close existing gas infrastructure. Cleaner sources of flexibility such as demand response and storage will be critical, alongside mass deployment of wind and solar.

For emerging economies heavily dependent on coal power generation, including “giants” such as China and India, but also the Philippines, Mongolia and many other countries, any shift to gas to replace coal will need to be short and temporary. The bulk of their transition will be straight from coal to clean.

For countries already highly dependent on gas for power generation, and where coal is marginal – including most Gulf countries, North Africa or post-Soviet countries – a “coal-to-gas switch” is not even a short-term option. The only way to further decarbonise would be switching to cost-efficient low-carbon sources, smarter grids, coupled with energy efficiency measures.

For low-income countries, many of which are dependent on distributed oil-based power generation, low-cost renewables play the biggest role in meeting growing power demand and delivering universal energy access by 2030. Gas is limited to a marginal role. Strengthening power grids, expanding off-grid solutions and developing new sources of flexibility will be critical.

In the buildings sector, fossil fuel boilers are phased out by 2025, alongside widespread energy efficiency retrofits and measures to ensure new buildings are net-zero compatible. By 2040, half of existing buildings are retrofitted to net-zero standards, rising to 85% by 2050. Half of heat demand will be met by heat pumps by 2045. This change is an enormous shift for gas-dependent countries in colder climates, such as Europe, North America and China. Gas distribution companies and boiler manufacturers will need to change their business models, while the building retrofit wave will create new jobs and a strong need for skilled construction labour.

Industry emissions fall by 95% by 2050 in the net-zero pathway, following rapid research and demonstration efforts over the next decade. The circular economy, industrial efficiency, electrification, hydrogen, and carbon capture, utilisation and storage all play important roles in displacing unabated gas from the industrial sector. Gas does not disappear entirely – it may still be used as a feedstock for some chemical processes – but its overall use is constrained. Countries such as India and China that had previously expected to massively expand gas use for industry will need to move directly to cleaner industrial production from electricity and hydrogen instead.

Shifting global financial flows

Reaching net zero requires a massive shift in investment. Oil and gas dominate global energy finance flows. Clean energy investment represents less than 40% of the total.

By 2030, clean energy investment will need to quadruple to more than $4trn (€3.29trn) a year to massively ramp up wind and solar power capacity and strengthen power system infrastructure including storage. Meanwhile, investment in oil and gas declines to a third of current levels as new gas exploration is discontinued and the role of gas shrinks.

The direction of travel for private and public finance is clear: the global energy industry will need to reorient its portfolios to renewables, transmission lines, storage and low-carbon fuels.

Historically, public financial institutions have been important investors in gas extraction, infrastructure and power generation, and help to de-risk private investment. The net-zero pathway will add to pressure on public financial institutions to fully phase out unabated gas lending.

Similarly, private finance and financial regulators will need to recognise the systemic risks of over-investment in gas, especially stranded asset risks. The report strengthens the case for excluding gas from the EU Sustainable Finance Taxonomy and similar measures elsewhere for classifying green investments, and for placing more focus on financial disclosures. For private finance, the IEA report is likely to accelerate the capital flight away from the gas industry.

Geopolitical consequences

Bringing the world onto the net-zero pathway will cause fundamental (geo)political shifts. It will bring forward new leaders in low-carbon technology and production value chains, create frictions related to critical materials, and challenge the global position of fossil fuel-producing countries.

Although the IEA model seeks to minimise stranded assets, the pathway puts gas-exporting countries in a tight spot, as fiscal revenues fall along with export volumes and prices.

“Annual per capita income from oil and natural gas in producer economies falls by about 75% […] which could have knock-on societal effects. Structural reforms and new sources of revenue are needed, even though these are unlikely to compensate fully for the drop in oil and gas income.” – IEA

Developing country gas producers – including exporters such as Nigeria and prospective new players like Tanzania – will be particularly exposed as revenues fall and new projects are abandoned. Without alternative revenues this could reduce state spending for health, education and other development purposes.

Russia’s transition will also be particularly difficult. Russia has only recently begun to expand its LNG exports, and remains highly dependent on pipeline exports to Europe. European gas demand will shrink the fastest, however, and alternative markets such as China will not replace the revenues lost from the European market.

Meanwhile, the global gas market is likely to centre even more around Asia and the Pacific for the next decade – although with far lower rates of growth than currently foreseen.

Economic diversification will need to become a top priority for major exporters such as Russia and emerging players like Mozambique, to lessen dependence on shrinking and volatile gas revenues.

Overall, global economic growth is higher in the net-zero scenario than under business as usual. The IEA highlights alternative economic opportunities that may ease the transition in fossil-producing countries. These include wind resources, green and blue hydrogen, critical minerals, and redeploying existing oil and gas expertise into technologies such as geothermal or CCS. However, the geographies of these opportunities are uneven, and countries with constrained financial resources may find it hard to pivot their economies.

Further downside risks for gas

While these numbers may seem stark for the gas industry, they are more positive than other 1.5°C scenarios that see gas use drop more swiftly.

In contrast to the drop in gas consumption in the IEA net-zero pathway of 3% by 2030 and 55% by 2050, the IPCC foresees a decline of 35–40% by 2030 and 60-80% by 2050. Similarly, UNEP’s ‘Production Gap’ report sees gas falling by 3% every year from now.

Faster technology changes may also further challenge the role of gas. Higher electrification means lower direct and indirect uses of gas. The IEA net-zero pathway reaches 50% electrification of the economy by 2050. This rate is more than double current levels, but well below the recent Energy Transitions Commission report which showed electrification levels reaching 70% by 2050.

Similarly, hydrogen plays a big role in the IEA pathway, but is split fairly evenly between ‘green’ hydrogen made from renewable electricity and ‘blue’ produced from natural gas with CCS. Analysis from the International Renewable Energy Agency shows green hydrogen beating blue hydrogen on cost by 2030 and continuing to get cheaper – which raises questions around the volumes of future gas demand for hydrogen production.

The IEA pathway is also highly dependent on CCS, including for gas use in industry, showing CCS capturing 4Gt of CO2 by 2035 – essentially from a standing start. Given the failure of CCS to take off so far, this presents a delivery risk. If less CCS capacity materialises, the space for gas will be even smaller.

Next steps

The IEA report signifies a global shift of the energy governance agenda, and for the first time puts the power of the agency’s energy analytics in the service of global climate goals.

There is still uncertainty about the future, but countries, cities, companies and investors can use the insights from the pathway to start their net-zero journeys. For governments, a host of policy changes will be needed to meet the 1.5°C milestones, from power market reform to building codes to industrial innovation and financial regulation.

The report will also trigger a reckoning in the gas industry and a host of related sectors from boilermakers to utilities to commodities traders: they will need to rapidly transform their business models to continue to exist in a 1.5°C-aligned world.

The new pathway also presents a challenge for gas-dependent countries – consumers and producers – to shift their strategies but for countries with limited financial resources, diversification is easier said than done.

Ultimately, success in reaching net zero will depend on managing the politics of the transition. Domestically, this requires setting clear phase-out dates coupled with just transition plans. Internationally, it requires richer countries and international institutions to mobilise investment and partnerships to support a stable transition, particularly for highly dependent gas producers and developing countries.

This article was originally published by Energy Monitor.