E3G has published a report on the political economy of climate-related financial disclosure in four target countries: UK, Germany, USA and Brazil. In these countries, the finance and investment landscape has been analysed across economic and political systems, as well as their external projection.

Purpose of this report

The Paris Agreement marked a watershed moment for tackling climate change. Post-Paris there has been a shift in focus from securing an international political agreement to implementing the low carbon transition. The political economy choices made around implementation of the transition will create clear winners and losers and represents one of the biggest challenges to achieving a well below 2oC future. While huge efforts have been invested in the technical analysis of the transition, to date very little attention has been given to political economy analysis. This report aims to address this gap with respect to implementing the recommendations from the Taskforce on Climate-Related Financial Disclosures (TCFD) by providing case studies in four key countries: The United Kingdom; Germany; The United States of America and Brazil.

The political economy of finance

The finance sector is deeply entangled in the politics of decarbonisation. Finance sectors tend to be a mature aspect of most countries’ economies – in contrast to new and rapidly growing sectors, such as digital and renewable energy. However, the role of climate change in finance in relatively new. This creates opportunities for innovation and competitive advantage, but finance institutions are also deeply entangled with supporting high carbon sectors. In many countries, large multi-national incumbents dominate the finance sector and will need to evolve to deal with climate issues. New entrants from the Fintech sector could lead to disruptive change, although to date their impact has been relatively limited.

Given the strong integration of finance across other systems within a country, analysing the politics of the finance system in isolation misses important linkages. It is therefore crucial to embed finance analysis in a broader context of the overall politics of decarbonisation. In particular, public-private finance dynamics can play a crucial role and vary markedly across different countries. As shown in Box 1 below, E3G’s Political Economy Mapping Methodology (PEMM) framework enables consistent comparison across different countries to examine the role of finance in terms of its economic significance, political weight and external projection.

Mapping the political economy of finance

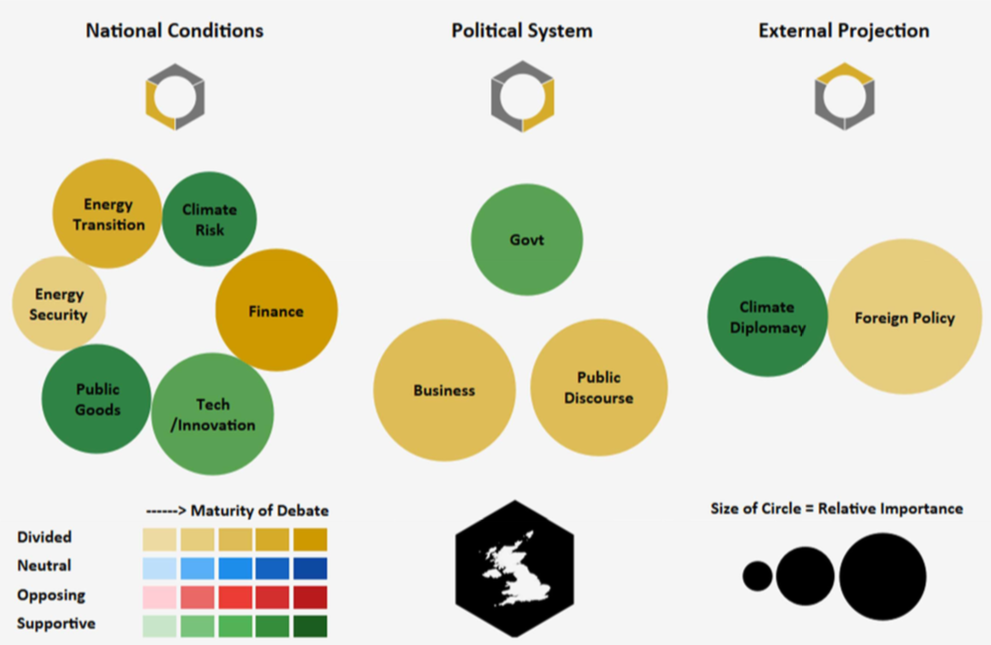

Political Economy Mapping Methodology (PEMM) is an analytical tool developed by E3G to assess threats and opportunities to countries presented by the low carbon transition. The three-dimensional assessment of national conditions, political system and external projection helps to determine what constructs a country’s core national interest and identify key national and international interventions which could help to increase domestic climate ambition and enable progress on the low carbon transition. The PEMM takes an iterative approach and combines hard analytical data, intelligence gathering, in-country testing and informed judgement.

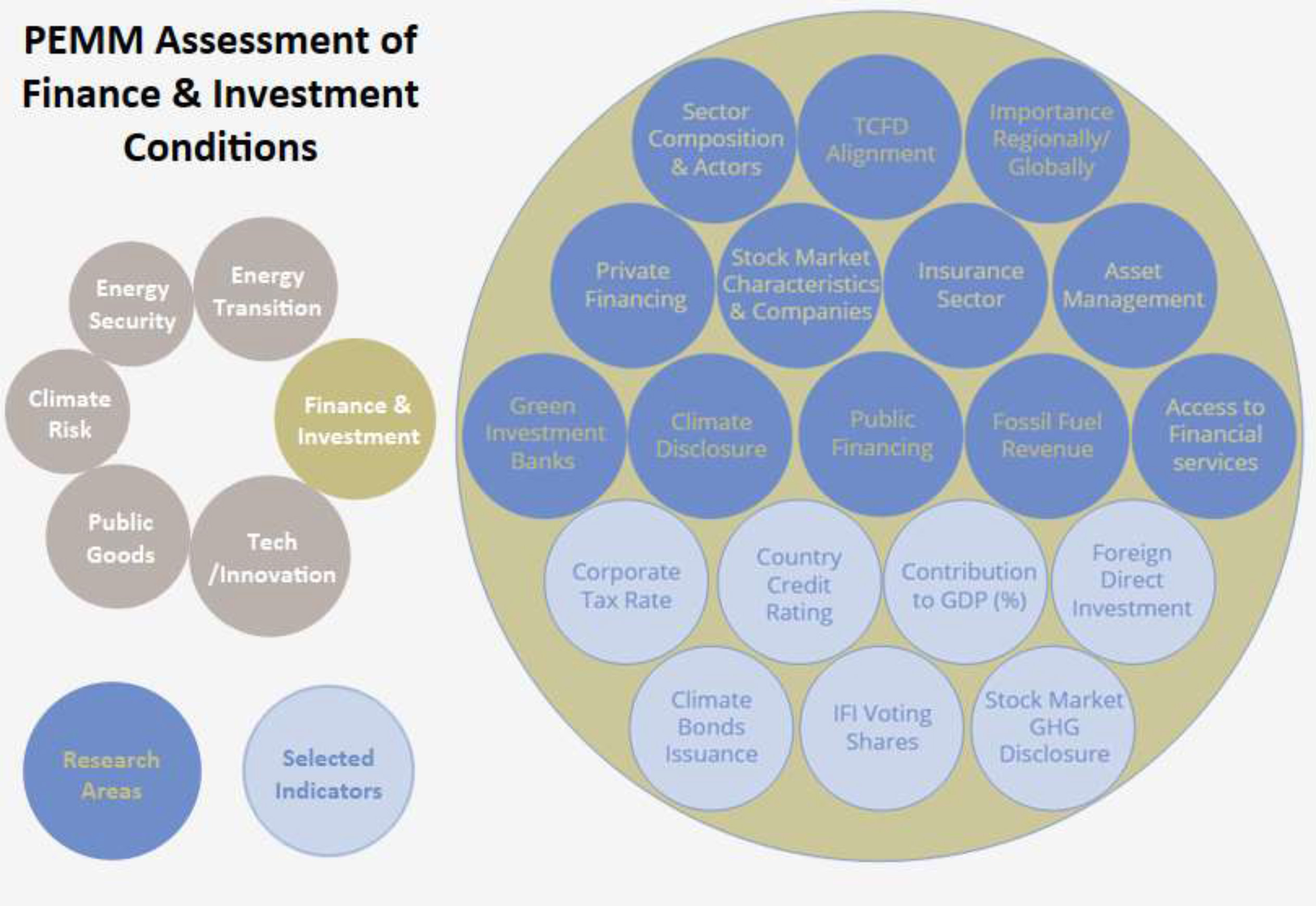

For the purposes of this report, the PEMM has been further developed to include an assessment of a country’s finance and investment landscape. The new methodology aims to understand how developed the finance system is within the economy; the key political actors involved and how the system is projected externally. As illustrated below, this is based on selected indicators, such as contribution to GDP and country credit rating, as well as broader research areas which require qualitative research and intelligence gathering, including the characteristics of public and private financing and governance mechanisms on climate-related disclosure. This information adds to the overall assessment of a country’s alignment with TCFD recommendations and the level of support for a low carbon transition.

Figure 1. PEMM Assessment of Finance & Investment Conditions

Country case studies: Key findings

By applying E3G’s Political Economy Mapping Methodology (PEMM) to these four key countries, we have identified initial conclusions and insights on taking forward climate- related financial disclosures. This analysis represents a first step in creating a broader political economy analysis for these issues. Further work will be necessary both to deepen the assessments and to broaden results to cover more countries. Nonetheless from the political economy mapping conducted in these case studies a number of key dynamics emerge as regards to furthering the implementation of climate-related financial disclosures:

United Kingdom

Deep divisions over Brexit dominate the political economy landscape in the UK. Securing future competitive advantage is the primary concern for most sectors. To the extent that climate change is viewed as supporting this agenda the UK will remain a global champion. However, pressure to secure new trade agreements with countries, such as the United States, could lead to a lowering of standards and risk a race to the bottom. Thus, while the UK is currently broadly supportive of climate-related financial disclosures, it is probably best characterised as a ‘distracted friend’:

- The finance sector dominates the national conditions in the UK, contributing to 6.5% of GDP and 32% of commercial service exports;

- The UK is simultaneously a champion of green finance and a major centre for high carbon fossil fuels. This includes active pursuit of new fossil fuel listings, such as the Saudi Aramco IPO, at the same time as initiating the Green Finance Taskforce;

- Brexit and the loss of passporting rights for the finance sector into the EU has led to concerns over competitiveness and the risk of business relocating to Frankfurt, Paris, Stockholm and Dublin. London’s leadership on green finance is seen as one aspect of maintaining its competitive position;

- Brexit uncertainty and a lack of legislative time for other issues has led to a dominant ‘wait and see’ narrative emerging on future finance legislation. The immediate focus of most stakeholders is on incorporating climate into existing regulation. Implementation of the TCFD recommendations will be viewed through a lens of future competitiveness and the Global Britain agenda, which could swing either way depending on whether they are perceived to provide an advantage or a burden;

- The UK has a number of high profile public champions, such as Mark Carney, Governor of the Bank of England whose term expires in 2019. It is not clear that the views of these individuals have been mainstreamed through their institutions, potentially leaving them vulnerable to change at the top;

- As the UK navigates its new position in the world post-Brexit, there will be a critical window to influence its long-term trajectory on climate finance. This could result in a race to the top with the UK playing a strong role alongside the EU and other countries on global standards. However, it could also lead to a race to the bottom if the UK tries to position itself as a low tax, low regulation hub alongside emerging financial markets like Dubai. How the UK relates to EU standard setting during any transition and post-Brexit will have a critical impact on long term European regulation.

Figure 2. UK PEMM Three-Dimensional Assessment

Germany

Following Germany’s 2017 general elections, the country experienced six months of prolonged party negotiations and failed attempts to form a government. A grand coalition government was eventually formed in early 2018, reducing political uncertainty but also exposing new political divides and growing polarisation. Germany is a champion of action on climate change globally, though it has a very conservative finance sector. Its primary political focus in finance is on Eurozone stability and associated reforms. This can lead to Germany being less progressive on climate disclosure issues internationally than it is on many other aspects of the climate agenda. As a result, Germany could be characterised as an ‘uncertain friend’ regarding TCFD implementation:

The finance sector in Germany is less influential politically than in either the UK or the US. Industrial sectors strongly linked to national identity, such as automobiles and manufacturing, have the most significant political economy weight. If TCFD was perceived to be increasing the cost of capital for these industries, it would lead to a strong political backlash;

- The heterogeneity of the German banking sector, with over 1000 credit unions providing finance domestically is an additional dynamic not seen in other financial sectors;

- Germany has been relatively slow in responding to climate disclosure issues domestically. Its finance industry and regulation is dominated by very conservative voices who are often reluctant to change. Some voices in the finance industry are actively aiming to slow down the implementation of TCFD regulations to give Germany time to catch-up;

- Frankfurt is looking to secure business switching from London post-Brexit but faces competition from other European centres such as Paris. Given the strong focus in France on implementing the TCFD recommendations, this may lead to an opportunity to create a race to the top in Germany. However, Germany also fears competition from New York and other centres who may not implement strong TCFD regulations;

- There are a large number of public banks (such as KfW) which suffered significantly from the financial crisis and are yet to fully recover. They also have significant investments in high carbon industries, especially coal;

- At the global level the German finance ministry is less ambitious than other parts of the German government. This complicates dynamics on climate disclosure at the German G20. Whether or not this will change under the new coalition government remains unclear.

Figure 3. Germany PEMM Three-Dimensional Assessment

United States

The election of President Trump in the United States has led to considerable volatility and deep division within the country’s national conditions, particularly on the energy transition, energy security and public goods. It has also created a more polarised political system, which is increasingly divided on the low carbon transition. The shift to an “America First” foreign policy and the decision to withdraw the US from the Paris Climate Change Agreement has also had a strongly negative impact on its external projection and positioning, despite progressive action taken by individual US states and non-state actors. The US is a leader on global finance, though considering its tendency to limit regulation it would make it difficult for the US to advocate and carry the message around TCFD implementation. As such, it would be characterised as a ‘divided actor’ with strong forces pushing in different directions:

- The US private finance sector is the dominant actor in global finance and it exerts significant political influence both domestically and in nations around the world. The US regulators are one of many global actors that set norms and standards, and US asset managers oversee about 60% of the global retirement market;

- US markets play a strong role both in climate finance innovation and in supporting high carbon investment, particularly oil and gas;

- The finance sector has traditionally sought to minimize regulation. Although there are important champions for climate-related disclosures, such as Mayor Bloomberg, the dominant position of the sector, even amongst climate progressives, is to avoid mandatory regulation;

- However, the US has a strong focus on activist investment from both public sector and private funds. These actors play a leading role in the development of new analytical tools to assess risks. Aligning climate-related disclosures with creating more efficient markets and better analytics could accelerate adoption;

- The Trump Administration is actively hostile to climate regulation and environmental and social governance issues. This is playing out both in the US’ position internationally at the G20 and in domestic regulation;

- However, sub-national actors, especially state and city governments, play a strong role in climate politics. Individual states, such as California, may be able to move faster in many areas than Federal regulation. The US is a leader in green municipal bonds, with $US 18 billion issued by sub-sovereigns since 2015.

Figure 4. USA PEMM Three-Dimensional Assessment

Brazil

Economic development and growth in Brazil has stalled alongside the nation’s most severe economic recession and high political instability resulting from one of the world’s largest anti- corruption investigations into political and business leaders. The focus on economic recovery has led to renewed interest and foreign investment in offshore oil and gas resources, creating national conditions and a political system that strongly oppose a low carbon transition. It has also elevated the importance of Brazil’s high carbon assets in international trade, leading to greater divergence between Brazilian foreign policy and climate diplomacy. Despite the economic and political weight of Brazil’s finance system, both nationally and regionally, the increasing role of public finance and Chinese foreign direct investment (FDI) into the most polluting sectors could create conditions where stronger disclosure requirements lead to the displacement of carbon-intensive financial assets out of the more transparent private sector into the less transparent public sector. In this context, Brazil would be characterised as ‘a lever not worth pulling’:

- Brazil’s finance sector is highly entangled with the government and carbon intensive business, especially agribusiness and oil. The state is reliant on oil revenues to remain solvent and oil is key to financing national social development programmes;

- Brazil’s finance landscape is dominated by public banks (55% of total loans are from state-owned banks) and Chinese FDI. China is one of the largest investors in Brazil, particularly in oil and gas extraction. There are currently limited opportunities to attract other investors into low carbon sectors in Brazil;

- Economic vulnerability owing to the recession has created an entry point for more FDI into fossil fuel development and a greater role of public finance institutions. Loans from public banks increased by 20% since the start of the economic recession and foreign firms are responsible for about 21% of domestic oil and gas production;

- The current environment makes TCFD implementation challenging. To the extent that it could be positioned to help drive greater investment in the economy there may be some appetite. However, this will need to be linked to more fundamental governance and anti-corruption reforms in order to have a sustained impact.

Figure 5. Brazil PEMM Three-Dimensional Assessment