In 2015, Chile set itself a target to reduce greenhouse gas (GHG) emissions by 30% per unit of gross domestic product (GDP) by 2030. This is enshrined in its INDC. A National Finance Strategy (NFS) is needed to enable Chile to meet its INDC through implementing its Climate Change Action Plan (Plan de Acción Nacional de Cambio Climático – PANCC) and meeting its targets both for mitigation but also adaptation by 2030. The Government has committed to putting this NFS for climate change in place by 2018 and is just at the beginning of considering how to develop it. In the first instance, there needs to be an agreement on what the framework for the NFS should look like – with a shared understanding of what needs to be financed, over what timeline, where the financing should come from and how it can be delivered. This document aims to provide supporting material to enable an NFS for climate change to be developed.

The Chile Challenge

Even if temperature increase is limited to 1.5°C Chile will face severe impacts on its resources and ecosystems. The country is highly vulnerable to the impacts of climate change, and shows features of the 9 vulnerability criteria established by the United Nation Framework Convention on Climate Change (UNFCCC), including low costal level throughout its territory, arid and semi-arid areas; areas prone to natural disasters; areas prone to drought and desertification; and areas with fragile ecosystems, including mountain ecosystems. Many of these features will impact economic productivity and need to be addressed when planning infrastructure. They will also have a material impact on agricultural productivity.

Per capita emissions in Chile are equal to the global average but have been rising in recent years. The energy industry is the largest contributor of emissions and electricity consumption and prices have been forecast to rise by approximately 30% over the next decade. The resulting need to decarbonise the electricity system can go in hand with the government’s aim of reducing electricity prices, increasing energy security by using domestic energy sources, as well as achieving its goals of increased energy efficiency and participation of renewable energy sources.

There are a wide range of national institutions, plans, policies, targets and initiatives related to both mitigation and adaptation underway in Chile designed to help achieve these goals. Many of these existing efforts are captured in Chile’s INDC which includes five pillars of action: mitigation, adaptation, capacity building and strengthening, technology development and transfer, and finance. Within Chile the overarching climate change planning in Chile is done by the PANCC.

While growth has slowed recently, Chile has been one of the fastest growing economies in the Latin-American region. According to the International Monetary Fund (IMF), Chile’s strong macroeconomic fundamentals mean the country is slightly better situated in terms of predicted GDP growth compared to other countries of the Latin-American region, which are all similarly dependent on commodity exports for income. The longer-term impact of the commodity price shock on Chile’s GDP will partly depend on the country’s ability to reallocate resources away from traditional support for mining and toward other productive sectors.

Climate change is highly linked to Chile’s economic situation and development. Adapting to climate risks and investments towards a low carbon energy system can have multiple benefits for the country’s development towards a smart, competitive, inclusive and resource efficient economy. As such, ensuring that climate and development agendas go hand-in-hand and reinforce each other will be an opportunity as well as a challenge when it comes to the implementation of national actions.

Finance sector and resources

A sharp ‘pulse’ of investment is required over the next 15 to 20 years to meet Chile’s financing needs, especially in infrastructure. For example, it is estimated that over USD 24bn will need to be invested in energy infrastructure alone. Current analysis suggests that this level of investment cannot be supported on the balance sheets of existing energy companies and utilities. It is also beyond the reach of public budgets. Therefore, private investors will be crucial in financing Chile’s INDC. Understanding and mapping where capital sits within the finance system as well as the risk appetite and return on investment needed by the institutions that deploy that capital is key to understanding how to develop an effective NFS.

Chile has one of the most well-developed private finance systems in Latin America and investment in clean energy in Chile was USD 8.5bn for the period 2009-2015, equal to growth of 162% over 10 years. Commercial banks, along with private equity, have traditionally been the ‘first movers’ on clean energy financing – notably through project finance. The ability of banks to price and manage risk – which is critical in the construction phase of new projects – and to blend different sources of finance means they are important financial players in the development of any NFS. Around one third of all banks operating in Chile are financing renewable energy projects including wind, solar and small hydro, accounting for USD 314m 2013.

While appetite appears to be increasing, bank participation in the sector appears much lower than in other countries of the Organisation for Economic Co-operation and Development (OECD) and with a narrower focus on large-scale projects. The low uptake has a variety of causes, including unfamiliarity with the technology, a lack of project finance skills, and the small size of projects. There is a case to be made for Government to work to widen the focus of the banks to look at smaller-scale investments as part of its NFS. Furthermore, much of the concessional finance offered to private banks is done through direct relationships with international development finance institutions (DFIs). While this makes sense in terms of establishing the market, looking toward the long-term a more strategic approach is needed. As part of moves to develop an NFS, consideration should be given to how DFIs can be involved in a more strategic discussion about targeted public finance offerings to the highest value areas.

Long-term institutional investors like pension funds will also be an important source of capital. Chile has the largest portfolio of pension assets under management in the Latin-American region, representing 69.5% of GDP. By 2050, assets under management could reach 90% of GDP. Chile’s pension system has been rated as having a sound structure in an international comparison, and has a significant volume of resources (USD 168.3bn) that could be invested in long-dated assets such as non-conventional renewable energy (NCRE). They can alleviate the pressure on public balance sheets – and the involvement of private sector actors in financing of projects are generally agreed to improve the quality of infrastructure projects by bringing private sector rigour to financing decisions.

National Development Banks (NDBs) have a key role to play in overcoming the investment gap both in terms of building confidence in stable policy regimes through the alignment of public and private financial interests and also in building capacity in low carbon investment. Their dual role is focused on complementing and catalysing the private sector through their insights into local opportunities and risks and also their relationship with the local private finance sector. In 2014, NDBs had contributed more than half of climate finance flows. For example, Nacional Financiera (Nafin) had an important role in Mexico’s 105% growth in clean energy in 2015 through one of the largest onshore wind energy portfolios globally at an estimated USD 2.2bn for 1.6GW. In Chile, NDBs have played an important role in promoting and shaping economic growth and increasing social and financial inclusion. Given that NDBs have been critical in promoting renewable energy investment and climate-proofing key sectors of the economy (including agriculture) there is a strong case to be made for putting them at the centre of the development of NFS.

Despite their relatively small size compared to the total amounts invested in Chile, the international climate funds are strategically important for a number of reasons, including for attracting private investment through enabling NDBs and Multilateral Development Banks (MDBs) to develop risk-sharing instruments and fostering learning and develop the technical capacity to deliver climate-resilient investment. Going forward the Green Climate Fund (GCF) could become one of the largest sources of international climate finance.

Real economy opportunities and challenges

While an economy-wide approach will be needed to facilitate Chile’s transition to a low-carbon and climate-resilient economy, the electricity sector and the agricultural sector are particularly important due to their respective potentials to both reduce emissions and develop climate-resilience.

Good progress has been made in decarbonising the energy sector and Chile recently put in place several specific renewable energy and energy efficiency targets. There has been a strong push in Chile to diversify its energy supply and Chile has become one of the top destinations for renewable energy investment. Installed NCRE capacity has more than doubled from around 5.5% in 2013 to 11.5% in 2015. The rapid growth of NCRE in the electricity mix can be attributed partly to the low cost of solar and wind technologies relative to fossil fuels and partly to the changes to the energy auctioning system, which enabled NCRE technologies to compete on a level playing field with fossil fuel power plants. The fact that some NCRE can compete without subsidies is a significant competitive advantage for Chile. But there is still a financing gap for energy infrastructure. It has been estimated that around USD 24.3bn needs to be invested between 2014 and 2023 in Chile’s energy infrastructure, mostly in electricity generation and distribution.

Solar photo voltaic (PV) and concentrated solar power (CSP) offer the largest development potential for Chile. The vast potential for and rapid growth of investment in solar makes it a strategically important resource for Chile. As such, it has been selected as a sector for which further analysis of opportunities and barriers to scaling-up should be considered more closely. The other sector identified as being especially interesting is geothermal – this is on the basis of its currently under-exploited but nonetheless significant resource potential.

Chile has been making progress on improvements to energy efficiency, and energy intensity has decreased 5% between 2008 and 2014. Policy efforts primarily include voluntary standards in place for industry and mining. However, Energy 2050 highlights that despite this progress, there is still much room for improvement.

A wide range of barriers will need to be addressed to meet the full potential for NCRE and energy efficiency. For NCRE deployment these include issues related to electricity grid connection and expansion, improvements to the regulatory framework, issues with land ownership, challenges for small-scale and distributed projects, and lack of awareness of financial instruments, among others. For energy efficiency they include insufficient or inaccurate information, the lack of track record in terms of market development, and uncertain revenues streams. These considerations should be taken into account in the development of an NFS.

With respect to adaptation needs, this analysis focuses in particular on the agricultural sector and broader issues of climate risk in the economy and infrastructure. While the agricultural sector has seen improvements in productivity growth and exports, challenges remain related to the sector’s socio-economic structure: 93% of the farmland is owned by 7.6% of landowners with property of 100 ha or larger. Because small farmers are particularly vulnerable to climate change, which compounds the inequality in access to resources, reducing vulnerability and increasing resilience is one of the Government’s main policy priorities. Generally, smallholders are essential for food security as they provide over 80% of the food consumed in a large part of the emerging and developing world. Chile’s main climate change vulnerabilities and related needs for adaptation and resilience include decreased water availability and increased extreme weather events, including floods and droughts. A key component of a risk management strategy should include ensuring access to insurance against losses. This year, a new Department of Integral Risk Management to Address Climate Emergency is being created, which will specialise in risk management to address problems of climate disasters in agriculture with a particular focus on smallholders.

In addition to the impacts it will have on the agricultural sector, climate change also poses risks to the wider economy and infrastructure. While early alert response for disasters has been good and has helped minimise losses, recovery is still an area where further work is required. From 2000 to 2009, there was on average a natural disaster every two years, with a cumulative economic cost of over USD 1bn. In 2010, the “catastrophe of the year” resulted in a loss of about USD 30bn, equivalent to 18% of GDP. The approach to post-disaster recovery has been ad-hoc. A key element of developing an NFS should therefore be to develop longer-term risk management strategies and instruments to increase resilience and adaptive climate-resilient infrastructure.

Conclusions on moving forward to develop a NFS

What emerges immediately from the mapping, analysis and stakeholder engagement undertaken during the project is that the Government is already undertaking much of the groundwork to develop an NFS. For example the new PANCC (2017-2022) is already setting overall objectives and identifying key issues for developing an NFS. This should be commended. Going forward a clear framework is needed for the NFS development process. This should be focused on answering three obvious – but critically important – questions:

- What overall objectives need to be delivered?

- Who needs to be involved in achieving them?

- How will decision-making processes move forward?

For Chile, the overall objective is clear, as it is set out in the INDC – but some work still needs to be done to clarify and coordinate sectoral priorities. Key stakeholders have been identified through this work – and have signalled their willingness to work together to develop an NFS. The next phase is to determine how the decision making will move forward.

We set out five steps the Government can consider as short term actions to develop its NFS.

Step one. Identify sectoral priorities and facilitate institutional coordination

Chile has developed a comprehensive set of plans, initiatives and targets setting out how it will address climate change. The next step is to ensure coherence amongst all policy efforts related to climate change; as such, the integration of policy efforts to ensure coherence should be a core theme of the process of developing the NFS. In this way clashing policy objective and conflict created by areas of responsibility that are not clearly delineated can be avoided – and some progress with delivery ensured. Delivering an overarching policy framework setting out the integrated role of different sectors in meeting overarching climate-resilience goals will be the first step. Chile’s climate change law (which is currently being considered) could act as a cohesive top-down ‘umbrella’ framework to achieve this. The PANCC also provides an opportunity to streamline and further coordinate climate change policy objectives across the relevant sectors of the economy. Good institutional coordination will also be important. Many different ministries are involved in climate change policy making and delivery in Chile. This is quite right – but also underlines the importance that, with so many government departments, stakeholders involved, it is clear where lines of responsibility lie and how coordination will be managed on a strategic but also day-to-day basis.

Step two. Identify and set up working groups for priority areas

Complex problems can be best addressed by bringing key experts and stakeholders together to develop effective solutions. Working groups are a well-tested method for bringing such individuals and organisations together. Dialogue and consensus building between government, institutions and core stakeholders ensures a broad understanding of national climate objectives so that financing solutions can be developed. Dialogue should include a wide range of stakeholders (targeted as appropriate to the issue at hand) from key government departments, business, investment and commercial institutions, insurance companies, long term investors, microfinance and national and international development institutions. An inclusive approach offers a number of benefits including allowing capacity building to understand issues and opportunities and dynamism in solving problems.

Through this work we have identified three priority areas that the NFS should focus on in the short term. The suggested areas are: energy; climate resilience for agriculture and infrastructure; getting to scale on finance. In addition, suggestions for key issues to be discussed for each priority area and the stakeholders likely to be willing and able to engage in NFS-related dialogue are included.

Priority area 1: Energy

Ensuring the relation of new transmission and distribution grid matters both demand and NCRE supply and that project momentum is maintained – Stakeholders: Technical experts from the Energy 2050 working groups, including stakeholders from different sectors including public and private financiers.

Expanding and diversifying NCRE – Stakeholders: Ministry of Energy, Centre for Innovation and Support for Sustainable Energy (CIFES), Chilean Economic Development Agency (CORFO), academia, civil society, key industry representatives – both from companies and trade associations, such as ACERA– as well as the finance and investment sectors. Actors involved in the NCRE working group of the Energy 2050 process.

Promoting energy efficiency – Stakeholders: Ministry of Energy, Division of Energy Efficiency, Chilean Energy Efficiency Agency (AChEE), CORFO, key industry representatives – both from companies and trade associations, such as ANESCO (ESCO association), equipment manufacturers, international experts as well as the finance and investment sectors.

Priority area 2: Climate resilience for agriculture and infrastructure

Meeting agricultural adaptation and resilience needs – Stakeholders: Ministry of Agriculture (Agroseguros, INDAP, ODEPA, Department of Integral Risk Management), local government, insurance companies, commercial banks, representatives from the agricultural sector, academia, civil society, international experts such as CGIAR and World Bank who can show how cooperative approach and insurance instruments have worked elsewhere.

Managing natural disaster and climate-related risks – Stakeholders: Hacienda, Ministry of Environment, Ministry of Public Works, Servicio Nacional de Geología y Minería (Sernageomin), Ministry of Housing, Ministry of Health, ONEMI – Ministry of internal affairs and public security, MDBs, international re-insurers, international experts (including government and commercial experts on managing risk).

Priority area 3: Getting to scale on finance

Scaling up finance & connecting institutional investors to infrastructure investment – Stakeholders: Hacienda, Ministry of Public Works, Ministry of Housing, Ministry of Energy, MDBs, Chile’s Pension Funds, Superintendence of Banks, Central Bank, Chilean Chamber of Construction.

Addressing the aggregation challenge – Stakeholders: Hacienda, Ministry of Public Works, Ministry of Housing, Ministry of Energy, NPBs, MDBs, private banks, Chile’s Pension Funds, energy investors.

Step three. Develop and then test core propositions around key priority areas to build the NFS

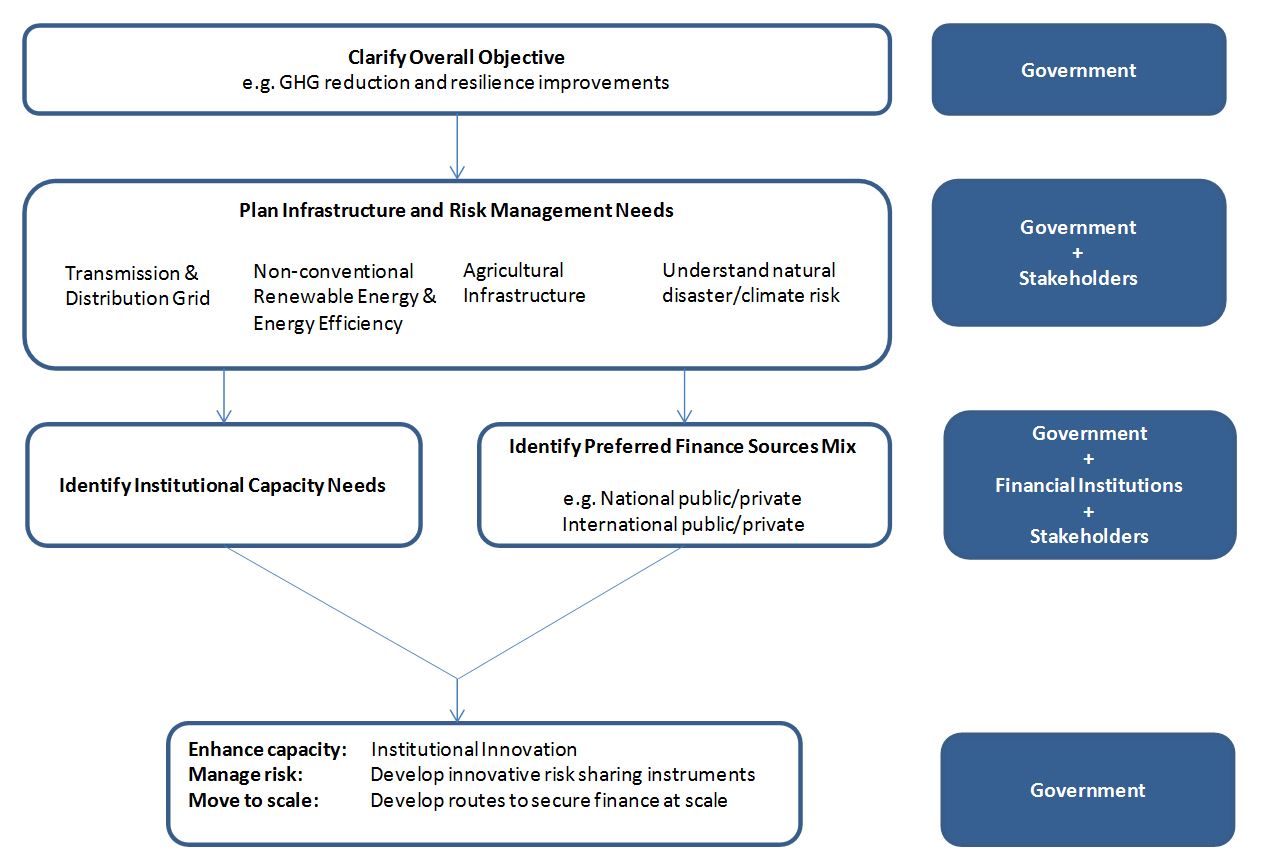

Based on the analysis undertaken (desk-top research, interviews with stakeholders and international experience), the following areas of focus for policy dialogue are suggested – as a means to develop core propositions that can be used to build the NFS. The figure provides an overview of how propositions can be developed and tested with stakeholders. It covers both steps 3 and 4 of the process described here.

Figure 1 Developing stakeholder-endorsed policy development processes

Step four: Seek wider feedback on emerging policy propositions

Once key policy propositions have been developed, it is considered good practice to then consult with a wider stakeholder community. Public consultation is a regulatory process by which the public’s input on matters affecting them is sought. Its main goal is to improve the efficiency, transparency and public involvement in large-scale projects or laws and policies. Feedback provided can then be considered by the Government as policy proposals are finalised.

Step five: Finalise policy proposals, draw together in a single document setting out the NFS plan and develop legislation as needed

Once policy proposals are finalised, the final step will involve taking the recommendations emerging from the NFS development process and work to implement them. This could take the form, for example, of the publication of a White Paper on unlocking long-term finance for building a climate-resilient Chile – with a set of regulatory and fiscal reforms to enable direct investment by domestic pension funds in NCRE and grid infrastructure or a White Paper on building a resilient agricultural sector that includes details of proposal to develop cooperative water sharing rights, a plan for investment backed by new public-private risk-sharing instruments developed with the GCF/MDBs/national public banks, and a new skills training programme using technical expertise from institutions such as CIFES.

From this process and clear “story”, the optimal mixture of institutional innovation/reform; policy initiatives and regulation; and financing instruments can be identified and delivered to achieve the overall policy objectives. The Figure below shows how the macro and micro level issues fit together and the role of Government and wider stakeholders in developing effective choices and solutions.

Figure 2 Policy objectives planning and implementation

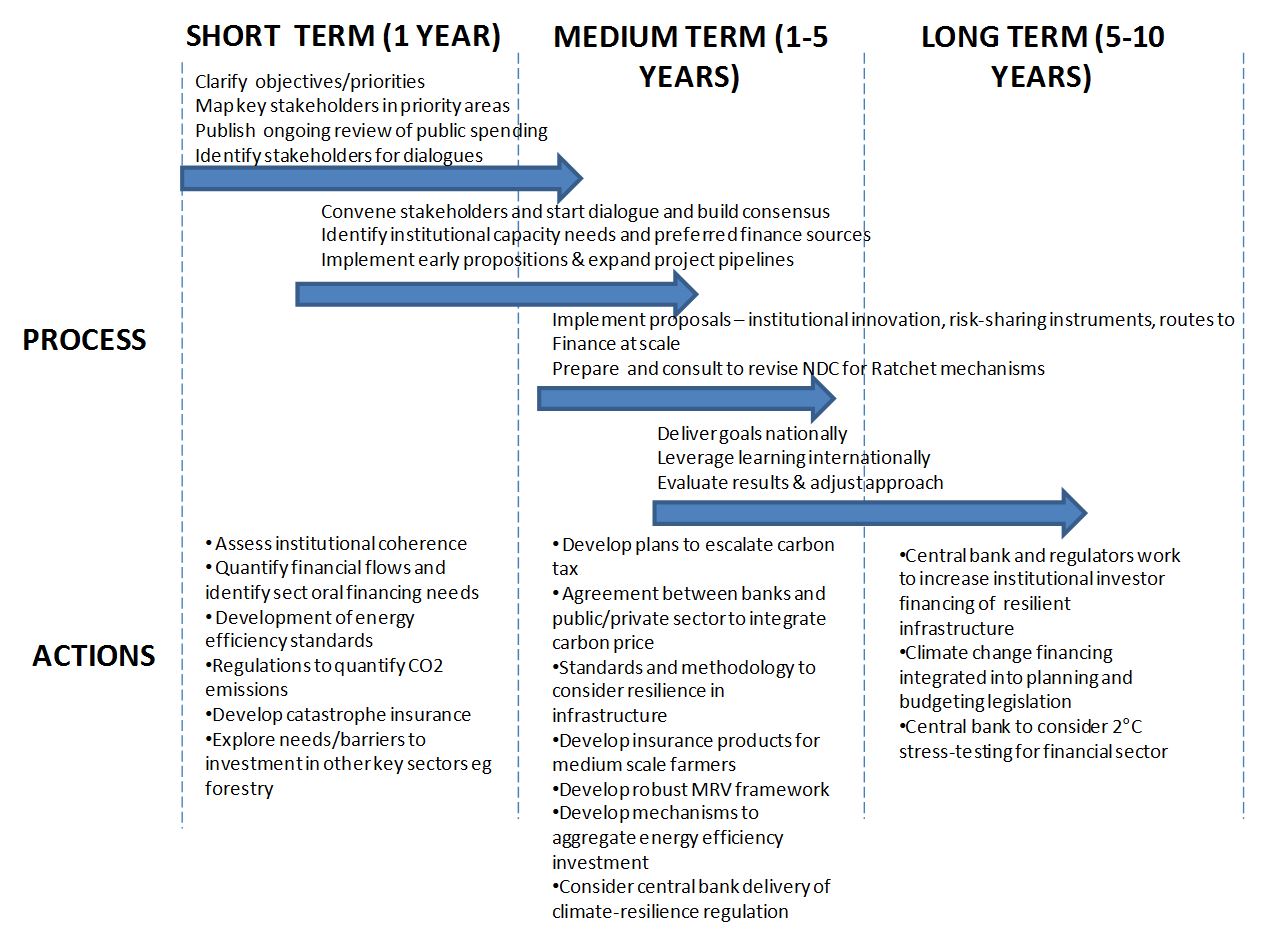

Medium and long term actions towards an NFS

Medium and long term actions should focus on implementing propositions so that the overall NFS goals can be delivered. In this way Chile’s obligation to deliver its NFS and its INDC goals can be fulfilled. The figure below sets out short, medium and long term actions.

Figure 3 Short, medium and long term actions towards an NFS

The opportunities and the challenges facing Chile regarding increasing investment in NCRE and energy efficiency and in improving the resilience of the agricultural sector are similar to those facing many other countries. Efficient decarbonisation of the Chilean economy (to meet some of goals of the forthcoming PANCC and deliver GHG reductions in line with the Paris Agreement) will mitigate the draining effect of increasing fossil fuel costs, promote security, competitiveness, investment and growth. Catalysing investment in sustainable agriculture and developing instruments and institutions capable of mitigating the worst effects of climate-related and wider natural disasters will do the same as they insulate the economy from event-related economic shocks.

Across the globe new innovations are pointing the way to how this can be best achieved through ‘greening finance’. Chile is now in a position to learn from this, use the insights to promote forward-looking dialogue with stakeholders and key national and international institutions, and develop an NFS that will enable Chile to build an inclusive, prosperous and climate-resilient economy.

Read the full report Considerations for a climate finance strategy in Chile [PDF 3.3Mb]

Leer el informe completo Consideraciones para una estrategia de cambio climático en Chile [PDF 3.3Mb]